We're teaming up with our friends at Sydecar to publish a three-part series on the legal (and non-legal) aspects of starting (and running) a venture capital fund.

Sydecar aims to bring more efficiency to private markets by standardizing how investment vehicles are created and executed. Their products allow capital allocators to launch investment vehicles instantaneously, track funding in real time, and offer hassle-free opportunities for early liquidity.

In Part I, we discussed the structures, players (GP, LPs, management company), and (some) key terms, including capital commitments, capital calls, and internal rate of return.

In this post, we will focus on some of the key terms related to starting and running a venture fund.

We organize these terms in two pockets:

Economic or Financial Terms

- Fund Expenses

- Management Fees

- Carry

Other Terms

- Thesis and Strategy

- Side Letters

- Alternative Investment Vehicles

Economic Terms

Fund Expenses

Starting and running a venture fund can be expensive.

Luckily for the GP, many fund expenses are paid out of the capital contributions of the LPs.

Fund expenses are the costs incurred for the day-to-day operation of the fund, including organizational expenses (e.g., the costs and expenses in forming the fund) and operational or administrative expenses (e.g., sourcing investments, legal fees), and accounting fees (e.g., tax returns, audits, financial statements).

Fund expenses do not ordinarily include expenses related solely to the GP, such as office space or salaries.

Fund expenses are paid directly from the LPs’ capital contributions, meaning that a GP does not invest the full amount of capital they raise.

For instance, even if the GP raises a $50M fund, that does not mean the GP has $50M of dry powder to invest, as a portion of the amounts raised will be used to cover fund expenses.

Also, it is important to note that fund expenses are separate from management fees.

Management Fees

Most VCs charge an annual management fee that is calculated as a percentage of the capital commitments of an LP over the life of the fund.

Management fees are payable by the LPs to the Management Company out of the capital contributions. The standard management fee in VC is 2% annually.

Regardless of how the VC chooses to call capital (whether all at once or (more commonly) through capital calls), the Management Company is entitled to take an annual management fee on the full amount of the capital commitments.

Management fees are ordinarily paid to the Management Company as compensation for its services.

The Management Company can use this pool of money to operate the fund and to cover the costs and expenses associated with its services (e.g., compensating employees, travel expenses, and other day-to-day expenses).

Similar to how fund expenses reduce the overall amount of dry powder, or cash available to be deployed into investments, it may not be advantageous for the VC to take the entire management fee.

For instance, for a $50M fund with a 10-year life, the aggregate management fees would be $10M–which may drastically cut the amount of deployable capital and, thus, the number of investments possible.

To address this, the limited partnership agreement (“LPA”) often provides that the management fees may be recycled (e.g., used to make investments)–thereby increasing the capital deployed and increasing the odds of generating a profit.

Further, because most of the VC’s activity occurs during the investment period, the management fee may be reduced in later years (e.g., drop by .5% for periods after the investment period or for all times after the investment period, be measured as 2% of the unreturned capital to the LPs).

Carried Interest and Waterfall

Carry or carried interest refers to the portion of the fund's profits that the GP is entitled to keep out of the distributions paid through the waterfall.

When the GP can distribute these profits to itself, however, can be subject to significant negotiations with the LPs and outlined in the LPA.

To better illustrate the GP’s entitlement to carry and distributions under the waterfall, let's look at an example:

In our example, the fund has received $25M in profits for its investment in PortCo 1.

If the GP can distribute, the LPs will receive $25M ($5M as a return on capital invested and $20M as 80% of the profit), and the GP will receive $5M (20% of the profit).

The key, however, is whether the GP can distribute the $5M to itself, which largely depends on the status of its other investments.

Let’s look at a few scenarios:

If the investment in PortCo 1 was one of a few exits and the other investments yielded returns of, say, $100M, then it is clear that the GP is entitled to distribute the carry.

Conversely, if all the other investments were marked down to zero, the GP could not take any carry (i.e., the total amount returned was only $30M of a $50M fund).

Those are relatively easy but unlikely situations.

Instead, what if none of the other investments had matured at the time of the exit of PortCo 1–could the GP take carry?

Typically, the LPA dictates that the GP can take carry on the exit from PortCo 1, so long as the portfolio's value on paper would still render the fund “in the money” for the purposes of the GP’s receipt of carry.

If it turns out that those paper marks were incorrect, and the final results were such that the GP would not have been entitled to take $5M as carry, the GP would need to return the money. This is called clawback.

Clawback may also apply if the distribution waterfall provided for a hurdle or preferred return and the final results of the investments did not clear the applicable threshold.

Hurdle Rate

Unless the Fund generates a return over a certain threshold (e.g., 6-8%), the GP is not entitled to take any carry.

Preferred Return

Similar to a hurdle in that it requires the GP to pass a certain annual threshold (6-8%) but also provides that the LPs receive all cash until that preferred return is exceeded, and the GP would only receive any carry above the preferred return.

Similar to the recycling of management fees, GPs are often entitled to re-invest a portion of the carry received on early investments (e.g., up to 120% of the capital commitments).

For instance, in our example, the GP could re-invest the $5M it received from the exit of PortCo 1 in hopes of generating even greater returns.

Other Terms

Fund Thesis and Strategy

GPs have considerable freedom in managing their fund and selecting investments.

However, the LPA does impose certain restrictions on their ability to make investments outside of a specified scope, typically outlined in the "purpose" clause.

Investment limitations can differ in scope.

For example, the LPA may broadly state that the fund will invest in "early-stage, privately-held companies," while others may be more specific, mentioning the stage, criteria, or industry (e.g., "venture capital investments in early-stage, privately-held companies focused on the healthcare technology").

The GP pitches LPs and raises the fund by describing its strategy and thesis.

Central to this thesis is the industry (e.g., B2B SaaS), stage (e.g., seed), check sizes ($500k-$1M), and portfolio construction (e.g., 65% initial investment/35% follow-on reserves) strategies.

LPs must evaluate a GP's thesis and strategy to ensure it aligns with their investment goals, as they are signing up for a blind pool of investments.

Side Letters

Side letters are agreements that grant additional rights to specific LPs.

These agreements are similar to those received by the VC from a portfolio company.

Side letters are usually only given to a select group of investors, such as the lead VC in a startup round or a prospective LP providing a significant investment.

Side letters may also be granted to attract certain investors or to manage regulatory constraints on an LP's investment, such as those imposed by the Employee Retirement Income Security Act (ERISA).

The content of a side letter can vary, but may include:

- Rights to more detailed information about each investment (e.g., its status and size)

- Reduced carry or fees (e.g., a waiver, reduction, or cap on management fees)

- Co-investment rights (e.g., the option for LPs to invest alongside the fund)

Alternative Investment Vehicles

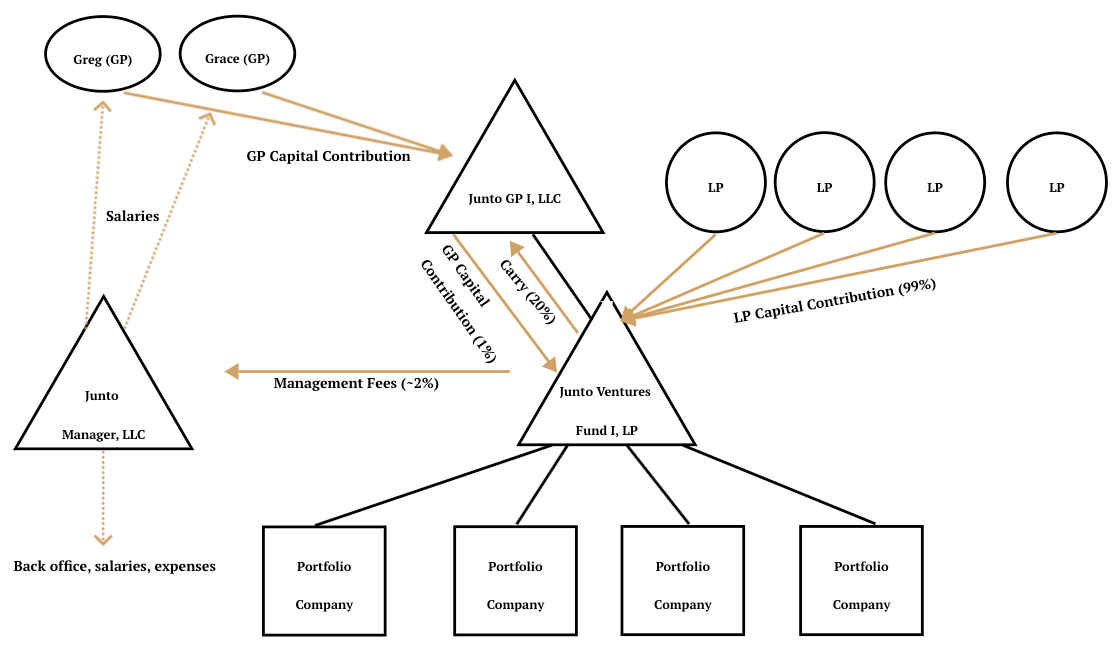

In Part I, we included a diagram of a typical venture fund (below).

Certain LPs may be subject to legal, tax, or regulatory issues that make investing in the fund untenable–unless certain special purpose vehicles (“SPVs”) are used.

The most common SPVs are parallel funds, feeder funds, alternative investment vehicles, and co-investment vehicles.

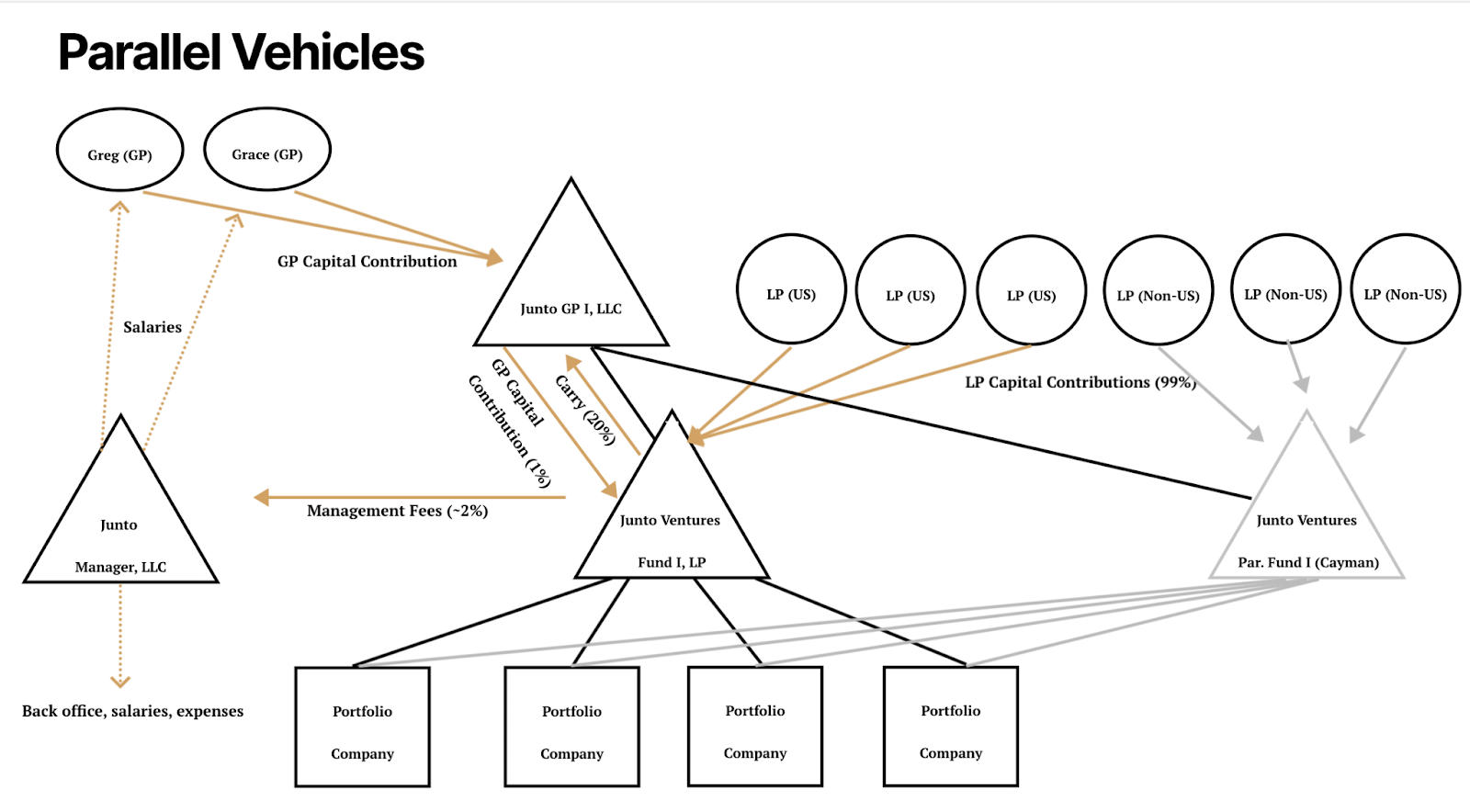

Parallel Vehicles

Parallel vehicles are typically established for LPs with a distinct tax status requirement that differs from other LPs.

For example, if a fund has non-US LPs, it may be beneficial to create a parallel fund in an offshore jurisdiction, such as the Cayman Islands, that is more favorable to these LPs.

Aside from specific legal, tax, and regulatory differences, the parallel fund will have the same investment strategy and terms as the main fund.

The parallel fund will also invest in the same assets simultaneously as the main fund.

The allocation into an investment will be pro rata between the two funds based on their respective portion of the total capital commitments.

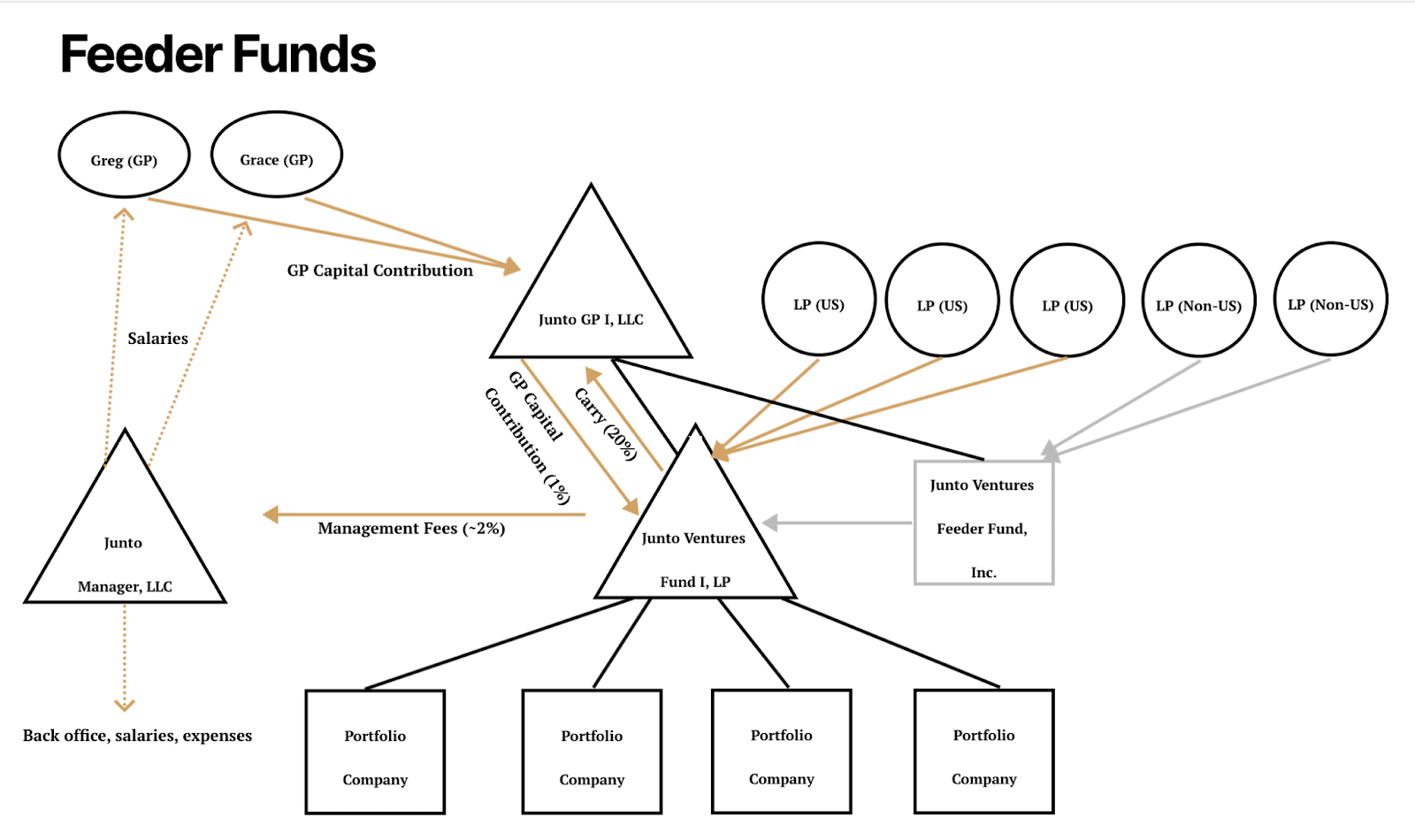

Feeder Funds

Another way to accommodate non-US LPS with unique legal, tax, or regulatory concerns is by using feeder funds.

A feeder fund is an investment vehicle organized as a corporate taxpayer.

Instead of investing directly into the fund, the LPs invest in the feeder fund, which then invests into the fund.

Because the feeder fund is a corporate taxpayer, it acts as a blocker in the relationship between the LP and the fund, as it will pay taxes on allocations and distributions–relieving the non-US LPs from filing and paying federal taxes in the US.

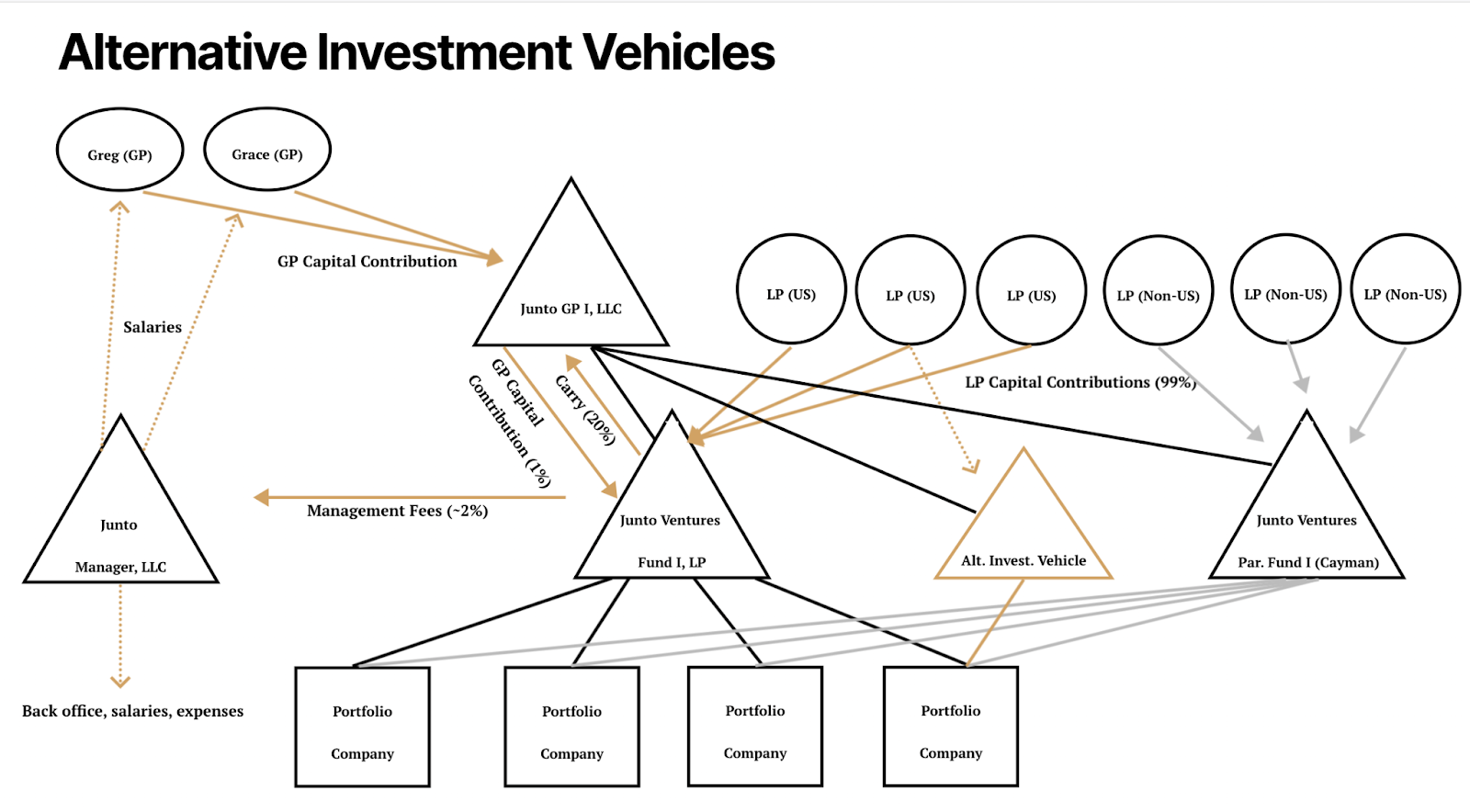

Alternative Investment Vehicles

Alternative investment vehicles are typically structured to address the legal, tax, and regulatory issues that may arise when certain LPs invest in a particular opportunity.

While a Parallel Fund invests alongside the main fund in each investment, alternative investment vehicles are limited to a single, specific investment.

In this way, alternative investment vehicles can provide a more focused approach for certain LPs, allowing them to tailor the investment to their specific needs and objectives.

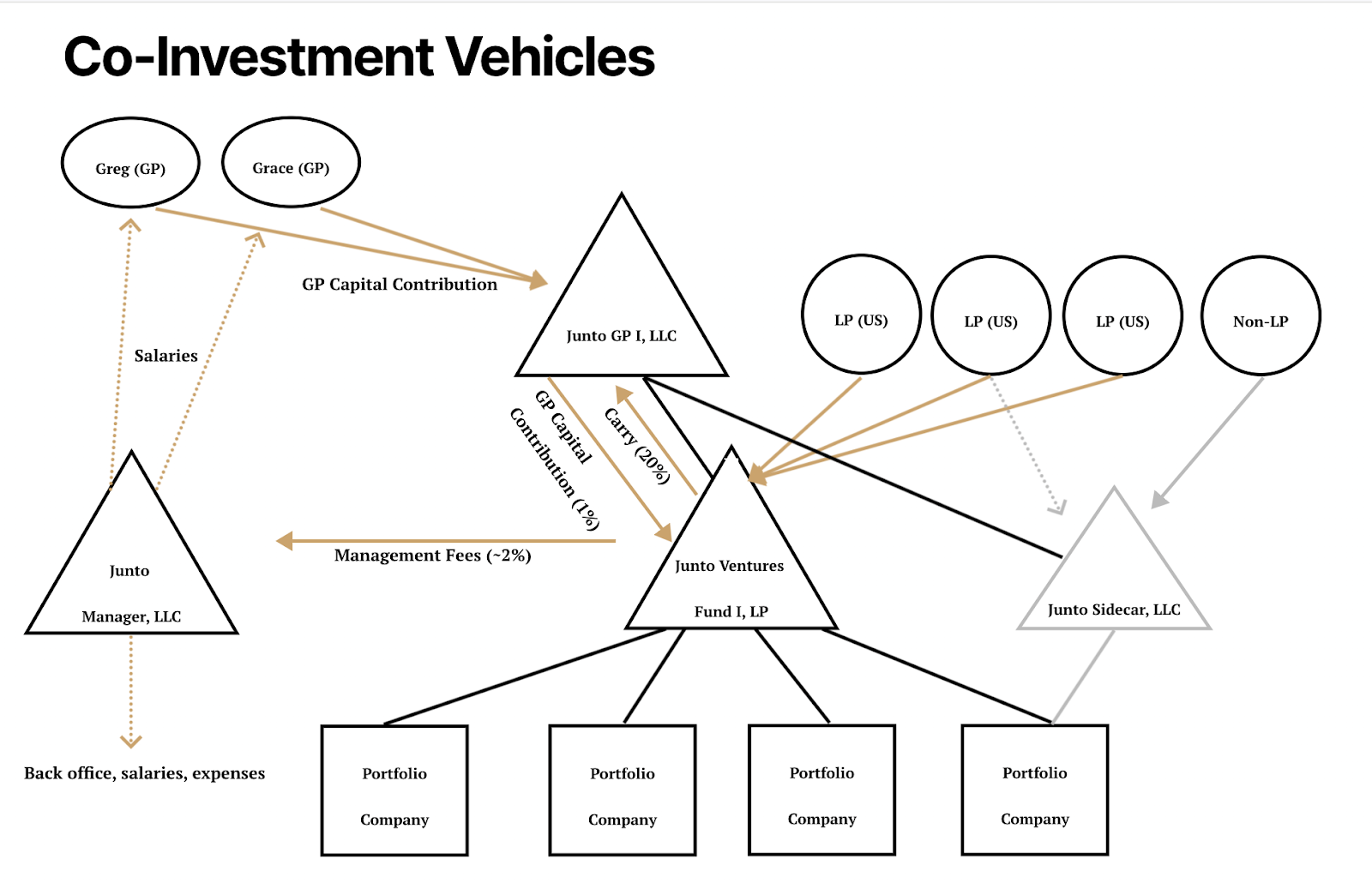

Co-Investment Vehicles

Co-Investment vehicles are SPVs created to invest alongside the fund on specific investments.

For example, an SPV may be used when the GP receives an allocation larger than the fund's limits.

In this situation, the VC may establish an SPV to invest the additional amount with one or more LPs or non-LP investors (i.e., investors that are not LPs in the Fund).

Summary

In this post, we provided an in-depth overview of the legal and financial components of starting and running a venture capital fund.

We also shed light on the expenses and management fees associated with the process and explained the concept of carried interest and waterfall.

The article further highlighted how the GP's entitlement to carry and distributions are determined through negotiations with the LP and outlined in the LPA.

About the Author

(and disclaimer)

Hey, if you like this article, you should follow me on Twitter (I tweet about venture, web3, and sports (with plenty of dad jokes)), check out what we are building, or set a time to chat.

Disclaimer: While I am a lawyer who enjoys operating outside the traditional lawyer and law firm “box,” I am not your lawyer. Nothing in this post should be construed as legal advice, nor does it create an attorney-client relationship. The material published above is intended for informational, educational, and entertainment purposes only. Please seek the advice of counsel, and do not apply any of the generalized material above to your facts or circumstances without speaking to an attorney.