We are partnering with our friends over at Angel School for a series of posts on all things venture investing.

In this post, Jed Ng discusses the benefits of angel investing through syndicates and the process of building your own network for syndicates. You can find the original post here.

Let's hear what Jed has to say.

I believe that syndicates are undervalued as an investment vehicle by the venture community. After all, startups talk about being ‘venture backed’, never syndicate backed.

AngelList which popularized SPVs, was only founded in 2010. Assure.co pioneered the first SPV admin service in 2012. That model made its way to Europe in 2018 with Vauban.

In the grand scheme of things, we’re only at the starting gate regarding syndicate and SPV adoption. As a result, there’s a lack of understanding of how syndicates benefit an Angel investor who can successfully build and run one.

Why I Know Syndicates Better Than Most

I started angel investing in 2016 and have backed two startups at seed stage that turned unicorn.

In 2020, I started building my syndicate. For the most part, I muddled through it because I couldn’t find structured resources. That forced me to look at the problem from a clean slate and examine every aspect of syndicate building.

In under three years, I grew an LP network from 0 to 1000+ with $0 spend, and I write cheques of $500k - $1MN today.

I also wrote a Syndicate playbook and founded AngelSchool.vc to help Angels build & scale their own syndicates.

The point is, it’s safe to say I understand syndicates as an investing vehicle pretty well.

A Framework for Valuing Syndicates

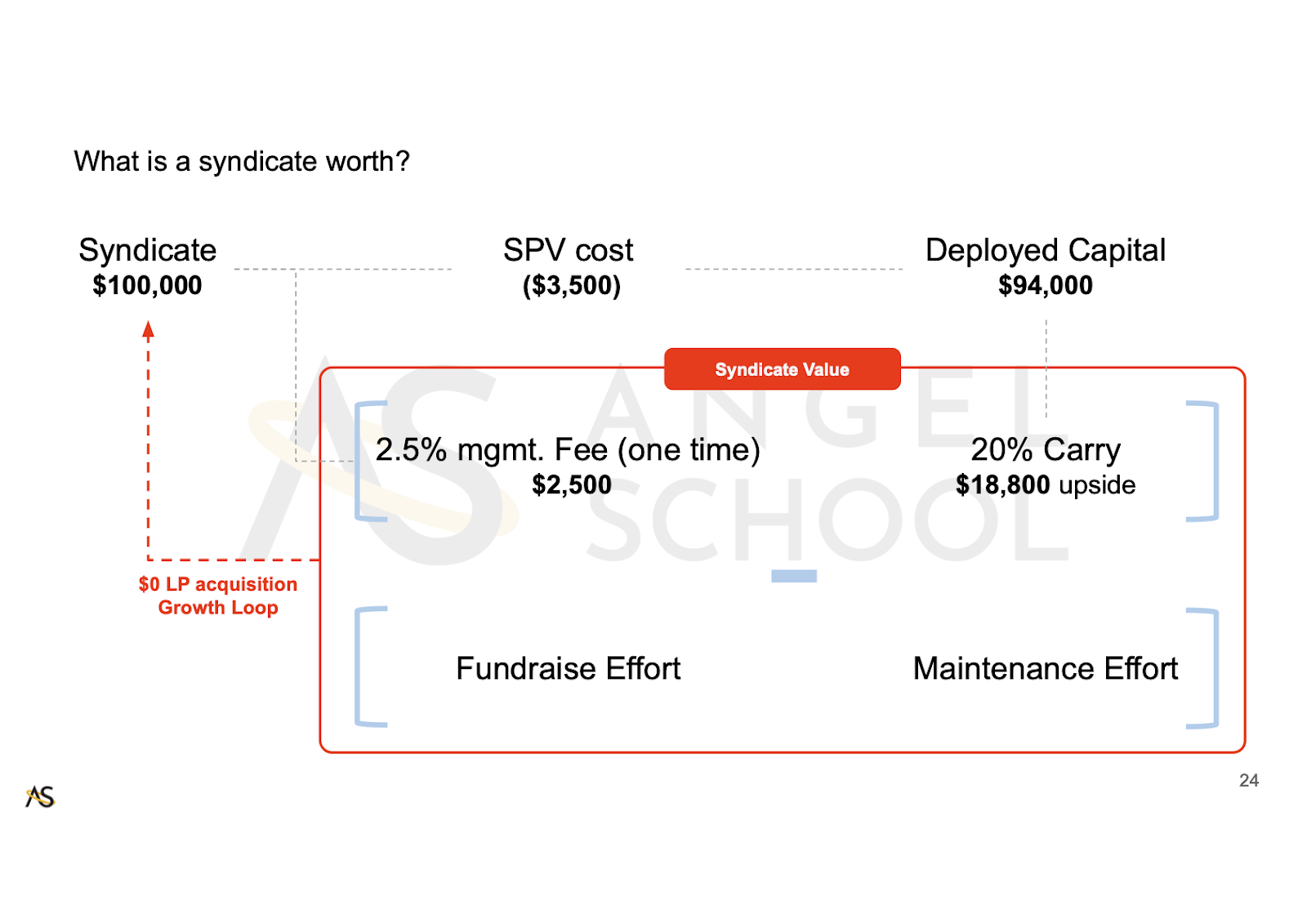

Let’s start with a framework for quantifying a Syndicate’s financial value from the perspective of the angel investor leading it. This is analogous to being a fund GP.

A Syndicate’s value is correlated with the capital it raises. This is driven by the size of your LP network, their engagement in your deal-flow, and their average cheque.

For each deal closed, the Syndicate lead might charge a management fee (in cash) and a share of the upside in terms of carried interest.

There are costs associated with putting the deal together, notably the cost of creating the SPV and maintaining it through the investment, and the effort of the Angel leading the syndicate for fundraising (due diligence, research and such) and maintenance, such as getting updates from the portfolio company and updating LPs.

Based on an economic structure of 2.5% management fee and 20% carry, a $100,000 raise generate $2,500 in fees and ~$19,000 of upside value for the syndicate lead.

This is diminished by the fundraising and maintenance effort.

The Argument for Syndicates

Syndicate leads can derive a number of benefits from running a successful one. There are advantages over being an individual angel and over fund GPs.

Here are the values that leading a Syndicate offers (and why i think every Angel investor and aspiring fund manager should consider building one).

Why Syndicates?

- Syndicates allow Angels to lever up on capital and earn carried interest. That means higher returns, or meaningful returns with lower exit multiples.

- Syndicates have a structural profit advantage over Fund structures. There are 2 reasons for this:

- No return hurdles

- Deal-level vs. portfolio-level carried interest

Syndicates have a virtuous loop through an LP growth loop. In other words, your LP network should grow on its own.

This growth loop means that your LP network → capital pool → carried interest upside grows over time.

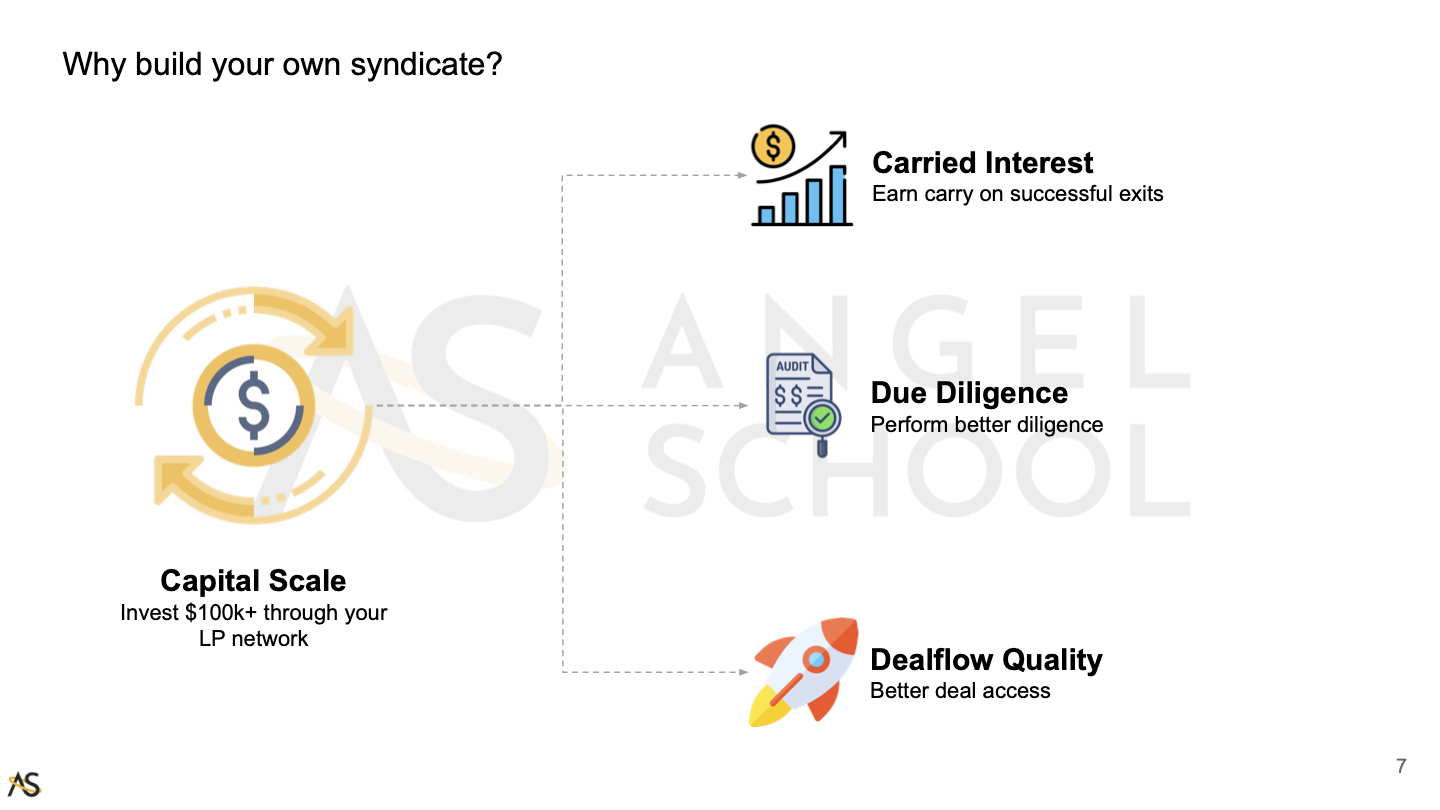

Scaling Capital

When you start angel investing and deploying capital, you’ll get to a point where it gets really expensive; you’re allocating too much capital to high-risk illiquid assets or both.

Syndicates allow you to access and scale capital in a short time. Being able to invest $100,000+ at a time through an LP network instead of financing every single deal off your balance sheet is like getting superpowers.

A larger potential check also entitles you to better due diligence. Writing a $100,000+ check instead of $10,000 - 20,000 will give you access to a lot more information.

You’ll also get better deal access and quality. These benefits improve the odds of your success.

The Carried Interest Argument

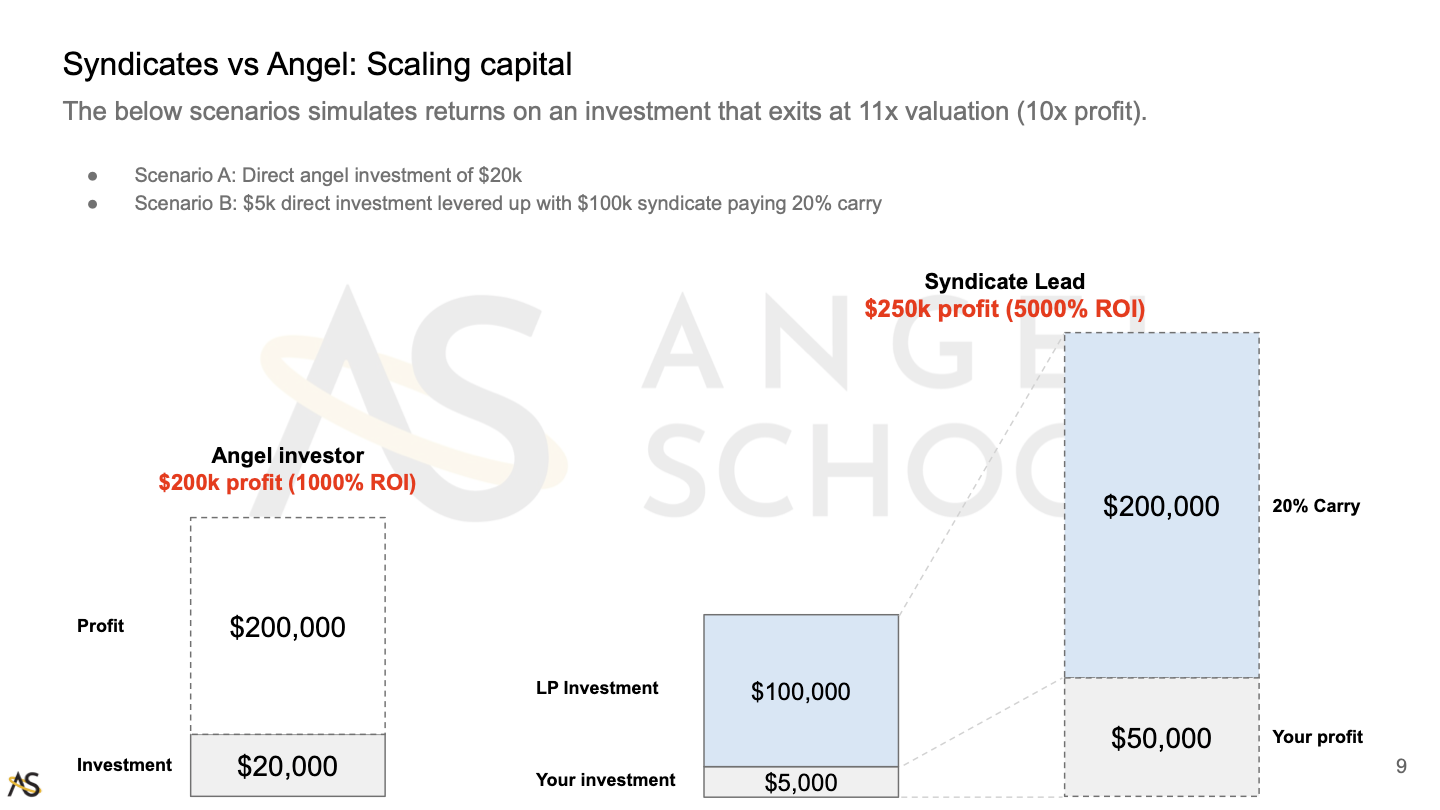

No doubt carried interest is appealing. Let's look at the math of carry and how that gives an Angel investor a bigger upside.

Let’s say you invested in a company, exited with a 10x multiple, and charged 20% carry.

As an angel investing $20k, you generate $200k of profit or 1000% ROI.

On the other hand, if you had a syndicate and invested $5k of your own money and raised an additional $100k of LP capital, you generate $250k profit on $5k capital at risk (5000% ROI).

Syndicate Profit Advantage over Funds

One of the more attractive and understated things about leading syndicates is that you have a structural profit advantage over VC funds.

There are two pillars to this argument:

- Carried Interest: Syndicates calculate carry on a deal level, whereas funds do so across the entire portfolio. As a result, portfolio companies that don’t return a profit diminish your total returns and, consequently, fund carry.

- Return Hurdles: VC funds have a return hurdle of 7 - 8% a year before any carried interest is paid out. This is to compensate fund LPs for the cost of capital. On the other hand, syndicates never have return hurdles.

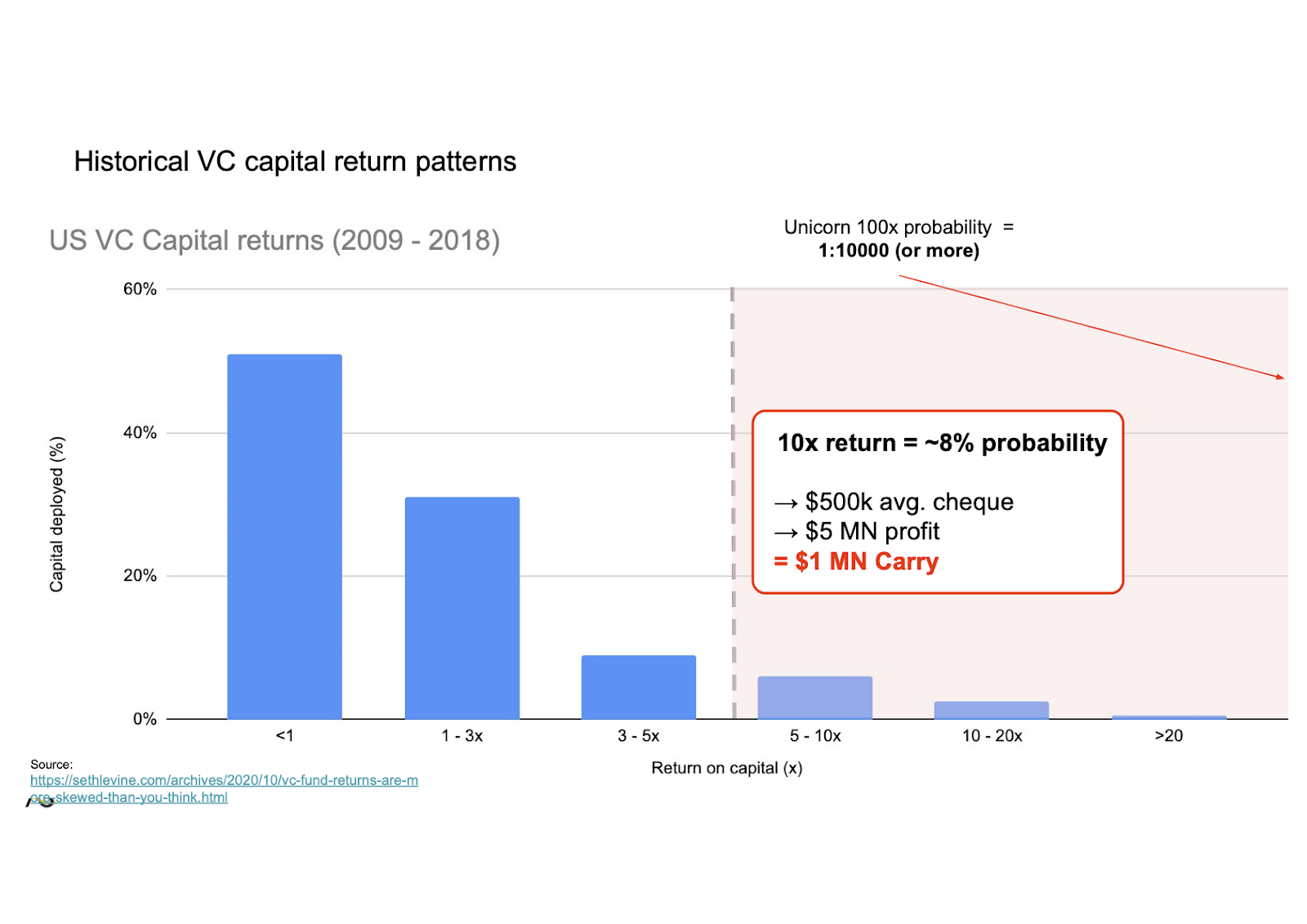

Let’s quantify this advantage using some market data.

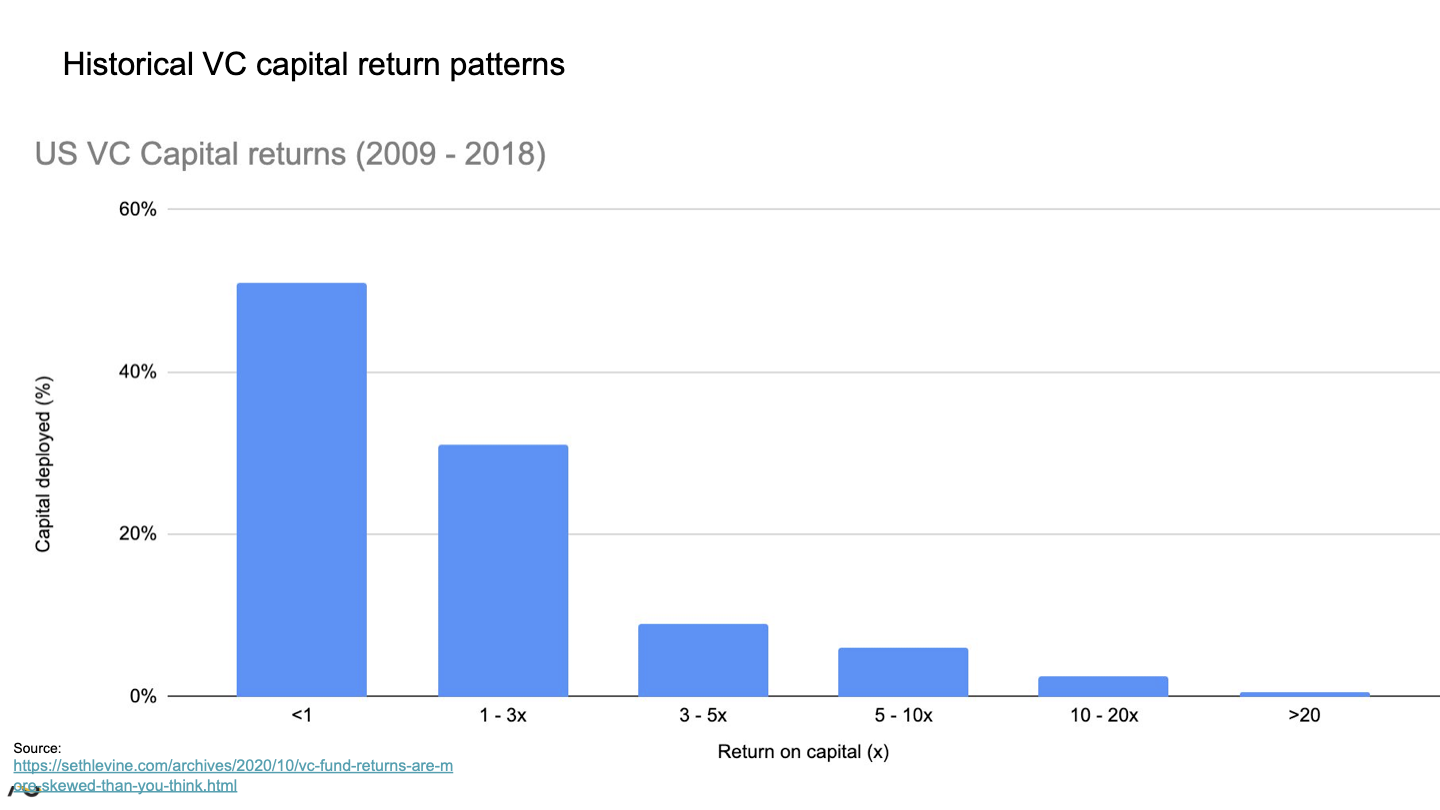

This histogram shows historical VC capital returns for a 10-year period. It’s a proxy for an average-performing investor.

The data tells us that ~50% of capital deployed returns less than 1x capital. 31% of capital returns 1 - 3x, 9% returns 3 - 5x and so on.

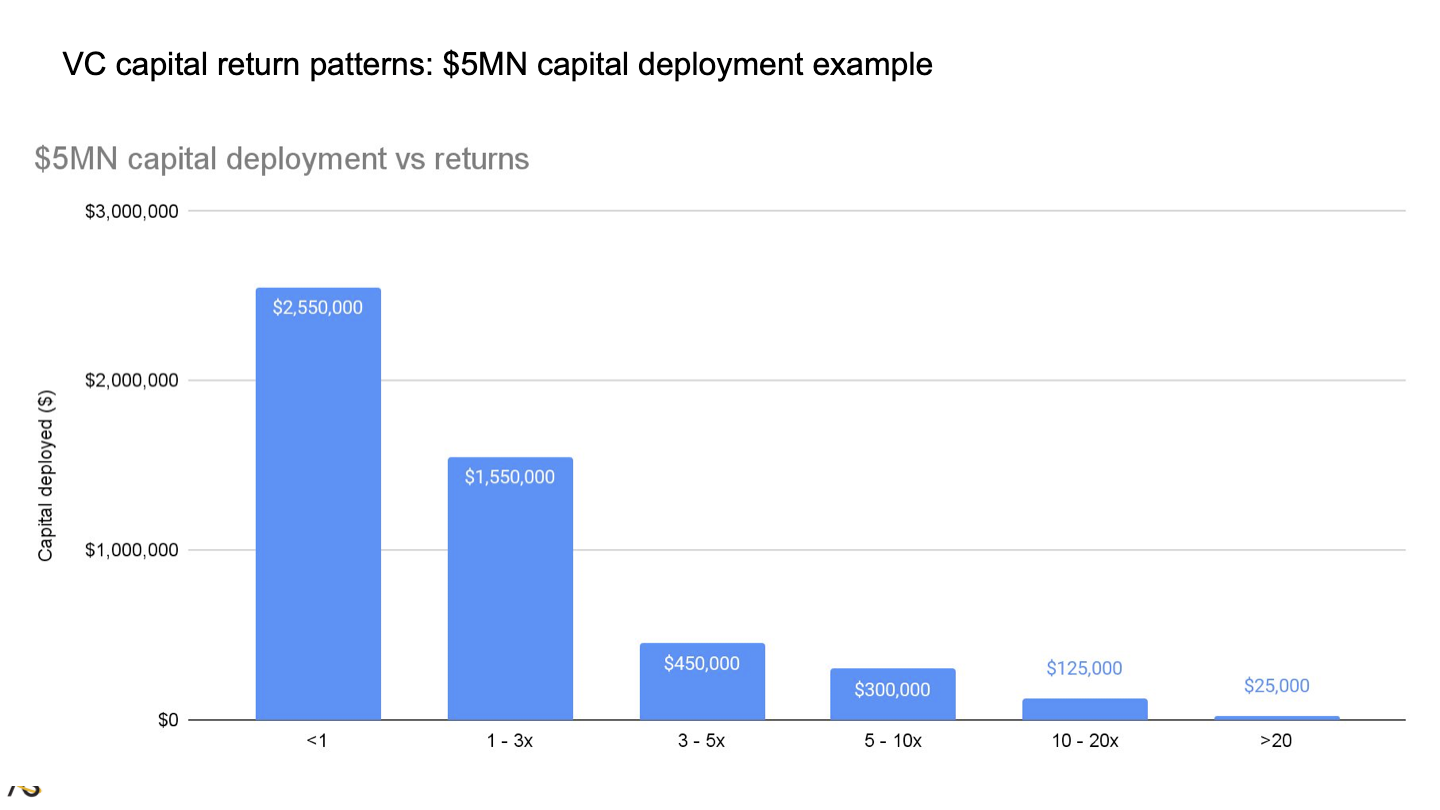

$5 MN of capital invested in this portfolio means $2.5 MN would've gone to a portfolio that returns less than our original capital.

$1.5 MN returns 1 - 3x. $450,000 returns 3 - 5x, and so on.

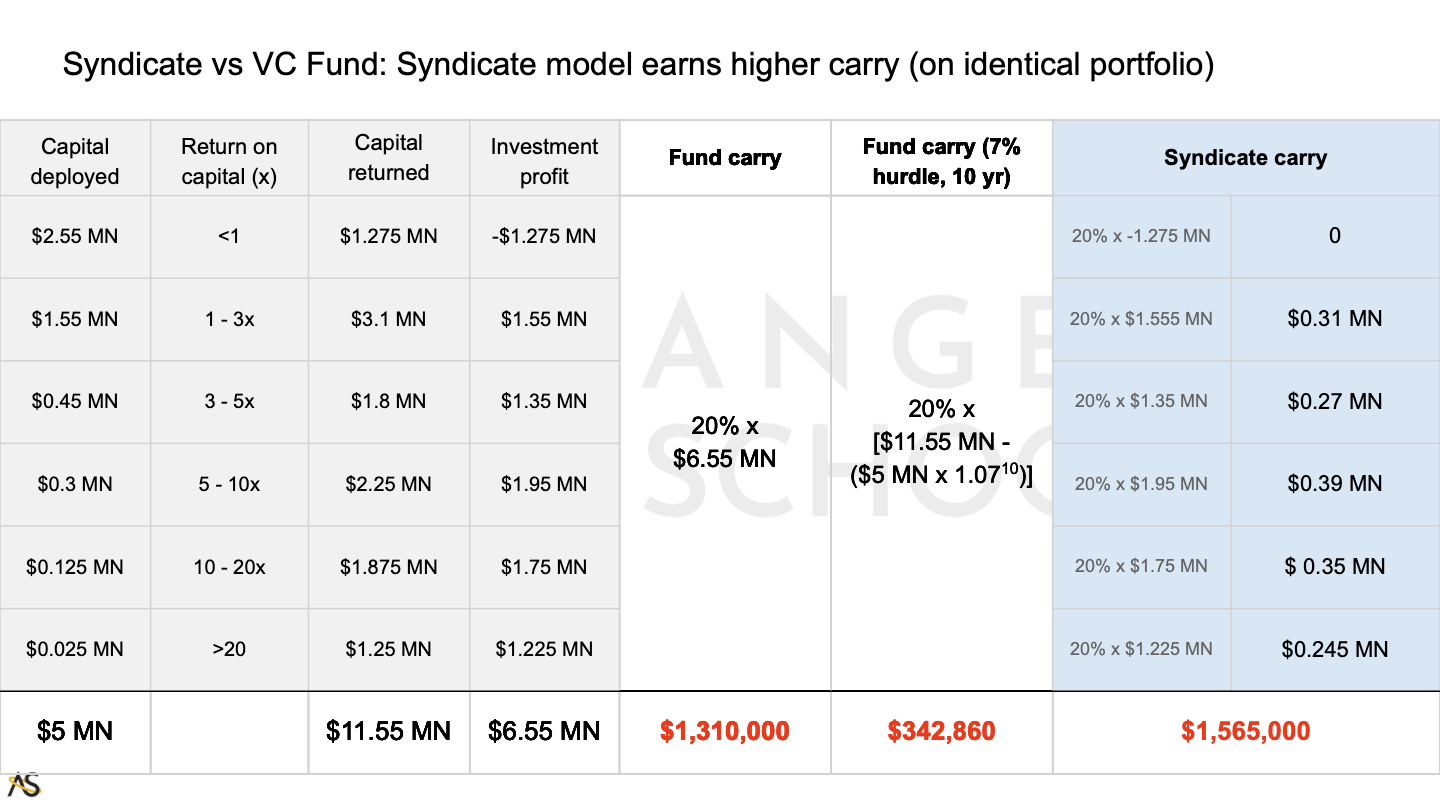

Here’s how the returns compare.

$5 MN capital deployed in this portfolio returns $11.55 MN, or $6.55 MN of investment profit.

A fund charging 20% carry, earns the GPs $1.31 MN of carried interest.

In the extreme (and improbable) scenario where the fund deploys $5 MN on day 1 and doesn’t return anything to LPs until year 10, the return hurdle diminishes carry down to $340k.

These are extreme outcomes, so it’s between $340k and $1.3 MN.

On the other hand, for syndicate leads, the portfolio losers have a floor of $0 carry (not a negative that carries across the entire portfolio). The syndicate lead actually generates the $1.5 MN.

This math scales proportionally with the capital deployed, so the structural advantage of syndicates can be substantial.

Of course, this assumes identical portfolios and the ability of the syndicate to marshall capital at the same scale as a fund.

The Syndicate Growth Loop

0 to 1 is always hard. There’s no getting around it. That applies to starting your syndicate as well.

The good news is that once you know WHAT to do, it’s simply a matter of execution. AND it gets easier as you grow.

Tapping into the syndicate growth loop is (scarily) simple. You simply need:

- A LP network at critical mass (100+ LPs)

- Engaged Investors who are paying attention to your deal-flow (I use metrics to measure this)

- Dealflow to generate those engagement metrics

Once those conditions exist, you’ll get a growth loop in the form of referral effects. Your LPs should be telling other angels about your syndicate or LPs sharing your deal-flow with others. I estimate this effect to be a 1% effect which is why you need at least 100 LPs to know if it’s just noise or actually happening.

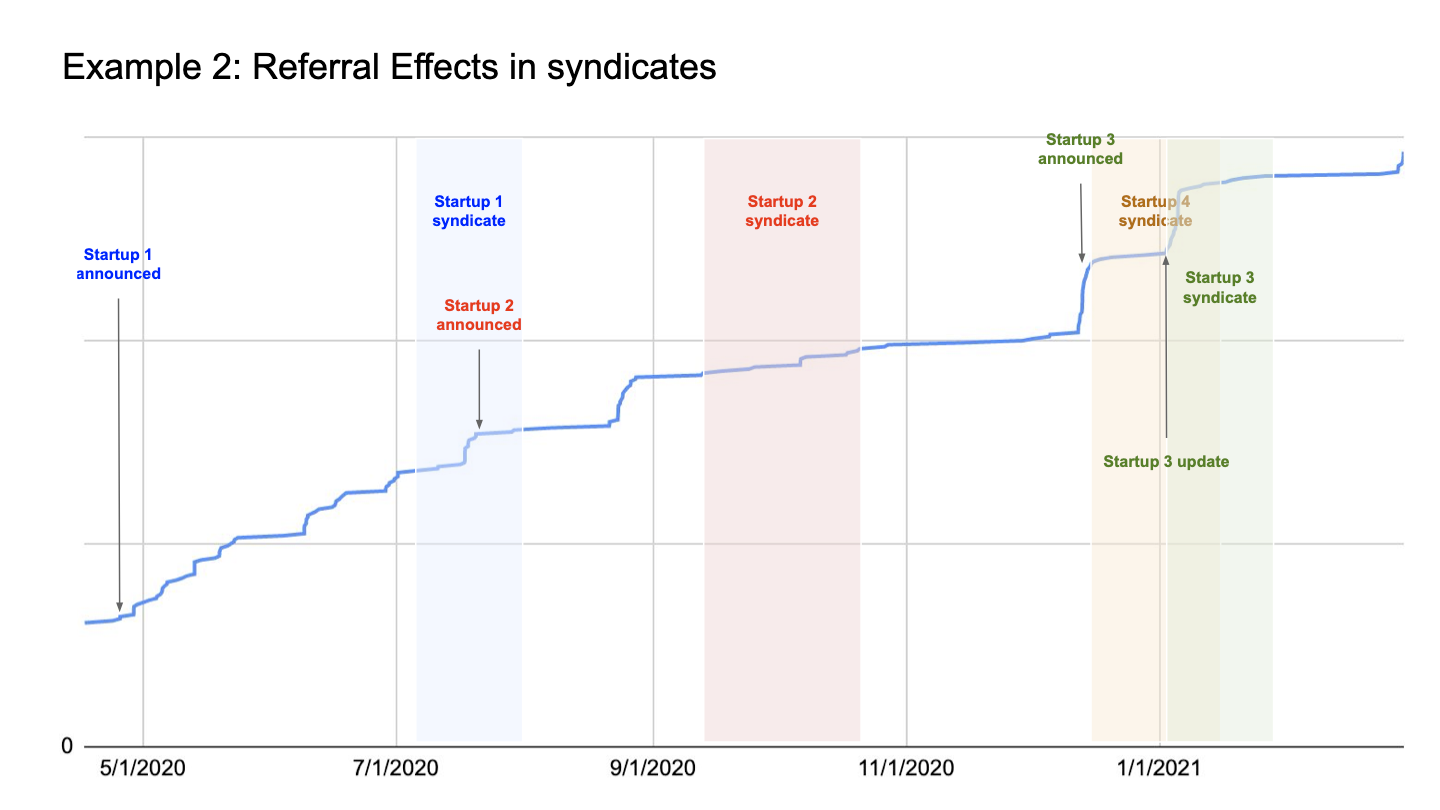

To prove this, I mapped my LP network (blue line) growth over time against my deal-flow activity.

The data shows a clear pattern between deal-flow activity and growth in the investor network. This proves a referral effect from deal-flow activity leading LP growth.

This is how I grew my LP network from 200 when I realized this pattern to 1000+ LPs today.

The Statistical Advantage Argument

This ability to grow your LP network on auto-pilot allows you to write larger cheques over time. This moves the odds in your favor even more.

The data on historical VC returns says that the odds of getting a 10x exit is roughly 8x. That’s a 1 in 12 chance.

Scaling capital allows you to get meaningful financial outcomes from modest successes.

A $100,000 investment that produces a 10x return for LPs means 20% carried interest is worth $200,000. Decent.

Growing that average cheque to $500,000 means that the Syndicate lead gets $1MN in carry on the same deal. We’ve gone from a nice bonus to a life-changing outcome!

You’ll also be doing multiple deals each year, each giving multiple shots on net. If you’re closing six deals a year, the math says you have a near-certain probability of getting that $1MN payout.

Value Syndiates in the Long Term

Syndicates are living entities. They need to built up and nurtured to grow over time. That’s why we need to take a long-term perspective.

Do the right things, and the upside compounds over time.

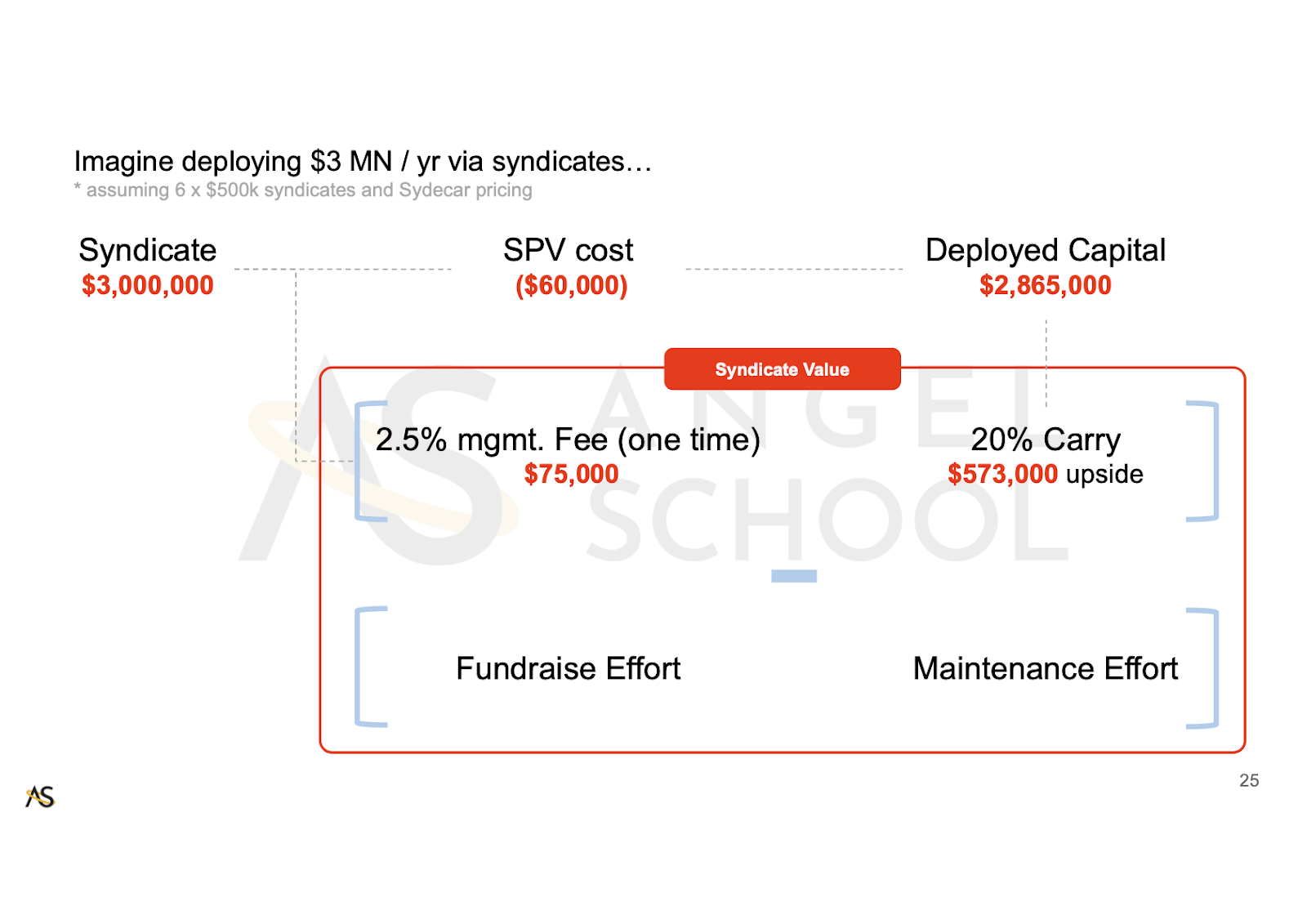

Getting back to our framework for Syndicate financial value. Let’s say you build a large, engaged network of 100s of LPs that back your deals.

The ability to invest $500k into six companies each year generates $75,000 in cash and $570,000 in upside.

It’s hard to argue about the value of getting your syndicate to scale.

About the Author

(and disclaimer)

Jed is the Founder of AngelSchool.vc - a program dedicated to helping angels build their own syndicates.

He has a track record of exits and Unicorns, and is backed by 1000+ LPs.

He previously built and ran the world's largest API Marketplace in partnership with a16z-backed, RapidAPI.

AngelSchool.vc is a Fellowship program dedicated to helping Angels build, run and scale their own Angel syndicates. We equip Program Fellows with our syndicate blueprint in their first eight weeks, and give lifetime access to our investment community and alumni network beyond that. Apply to our next cohort here.

Angel School’s syndicate is backed by a global Super Network of 1000+ Operator-Angels and deploys $MNs a year.

Disclaimer:While I am a lawyer who enjoys operating outside the traditional lawyer and law firm “box,” I am not your lawyer. Nothing in this post should be construed as legal advice, nor does it create an attorney-client relationship. The material published above is only intended for informational, educational, and entertainment purposes. Please seek the advice of counsel, and do not apply any of the generalized material above to your facts or circumstances without speaking to an attorney.