We're teaming up with our friends at Sydecar to publish a three-part series on the legal (and non-legal) aspects of starting (and running) a venture capital fund.

Sydecar aims to bring more efficiency to private markets by standardizing how investment vehicles are created and executed. Their products allow capital allocators to launch investment vehicles instantaneously, track funding in real time, and offer hassle-free opportunities for early liquidity.

You can read our first post on common structures and players and our second on venture capital fund's key economic and non-economic terms.

This post will focus on the legal and regulatory aspects of raising and running a venture fund, specifically, the compliance obligations and regulations that impact a VC.

Securities Act of 1933

The Securities Act of 1933 (the “Securities Act”) governs the fund's offer and sale of securities to LPs.

The SEC has used “investment contracts” to include a broad range of assets, contracts, instruments, and relationships as securities.

Given this definition, an offer and sale of interests in a fund should be considered an offer and sale of securities.

To properly offer and sell securities under the Act, the fund (also known as the “issuer”) must do so under a valid registration statement or an exemption from registration.

Given the regulatory and administrative requirements, registering fund interests is not practicable, so they are offered and sold through the exemptions offered by Reg D–commonly under Rule 506(b) and Rule 506(c).

Founders take note: Reg D 506(c) is bigger than the US IPO market. ⤵️

— Crystal Carson (@crystalcarson_) March 6, 2023

You can launch within days to raise capital. What’s needed?

1: Issuance platform contract

2: Subscription agreement

3: Landing pagehttps://t.co/L8aOPyvE75

cc @darrenmarble #issuance #regd #investors #fintech pic.twitter.com/puFXJcvRxJ

Rule 506(b)

Rule 506(b) allows a VC to raise capital from an unlimited number of accredited investors and up to 35 non-accredited investors (more on this later).

Generally, a non-accredited investor must be a sophisticated investor who can evaluate the economic risks and merits of the proposed offering.

What is an Accredited Investor?

The SEC summarizes the definition of "accredited investor" as:

One of the benefits of Rule 506(b) is the streamlined process of validating an LPs status as an accredited investor.

Under Rule 506(b), an issuer must reasonably believe an LP is an accredited investor.

VCs often satisfy this obligation by conditioning a subscription on receiving an investor suitability questionnaire providing the basis of an LP’s accreditation.

Despite the ability, many issuers do not allow non-accredited investors to invest in a Rule 506(b) offering because the issuer must provide more detailed disclosures (e.g., two years of financial statements and a more detailed description of the issuer’s business and the risks involved). If an issuer makes these disclosures to non-accredited investors, it must also provide such information to its accredited investors.

However, the biggest limitation of Rule 506(b) is the prohibition of general solicitations and advertisements.

Rule 506(b) offerings cannot advertise in the general media (e.g., tweet about the offering) or engage in cold outreach campaigns or solicitations (e.g., direct messaging a prospective LP on LinkedIn).

In practice, the issuer must have a substantive and pre-existing relationship with the prospective investor.

There can be a fine line between a substantive and pre-existing relationship and a general solicitation but use common sense. Do you have a relationship with this person? No? Well, then, that direct message is probably a general solicitation.

Rule 506(c)

For many VCs, Rule 506(c) is the more appealing exemption because it allows the VC to advertise that it is raising a fund.

This may be particularly important for VCs with large networks that want to leverage those networks to reach a broad base of LPs.

The tradeoff of this benefit is that Rule 506(c) is not available for non-accredited investors, and there are heightened duties on a VC to verify an LPs status as an accredited investor.

When using Rule 506(b), most VCs will require LPs to submit a statement from an attorney, CPA, or investment professional verifying the LP's status and/or require the submission of detailed financial information (e.g., tax returns or bank statements).

Form D and Blue Sky Filings

As part of a Reg D offering, VCs must file a Form D with the SEC within 15 days of the first sale (e.g., the initial closing) or a binding commitment to purchase securities (e.g., an accepted subscription agreement), whichever is earlier.

Form D requires the issuer to disclose certain information about the sale, such as the issuer's name, the types and amounts of the securities offered for sale, and the number of accredited and non-accredited investors.

Securities offered under Rule 506 are considered "covered securities" under the Securities Act, which means they are exempt from state-level securities laws, also known as Blue Sky laws. However, state regulators may still require issuers to file certain state notices and pay associated fees.

Fortunately, the North American Securities Administrators Association Electronic Filing Depository system offers electronic submission of Form D notice filings to participating state securities regulators.

Investment Company Act of 1940

The Investment Company Act of 1940 (“Investment Company Act”) regulates investment companies, such as those in the business of pooling assets from investors (e.g., mutual funds, private equity funds, hedge funds).

Similar to the reliance on exemptions under the Securities Act (i.e., Reg D), venture capital and other private equity funds typically rely on an exemption under the Investment Company Act, namely the exemptions under Sections 3(c)(1) and 3(c)(7).

The exemption a fund uses will depend on the nature of the fund and its LPs.

Section 3(c)(1)

Section 3(c)(1) is a common exemption for venture capital funds and exempts issuers that are not making or proposing to make a public offering of their securities and are limited to a certain number of investors.

For venture funds with less than $10M in aggregate capital contributions and uncalled capital commitments, the fund is limited to 250 “beneficial owners.”

For funds over $10M in aggregate capital contributions and uncalled capital commitments, the fund is limited to 100 “beneficial owners.”

This 100-investor limit has been questioned by VCs for years as the limit forces funds to focus on LPs that are capable of contributing substantial capital.

Yesterday I had the honor of testifying to Congress for a bill that would increase the limits of LPs into a Venture fund from 100 to 600. While many got to see my oral statement here is a copy of my longer written statement.https://t.co/Mdp5I4ka7v

— MacTheVC.eth (@MacConwell) February 9, 2023

This limit pushes funds to have higher minimum check sizes, making the investment inaccessible to investors with less available capital.

When counting the number of beneficial owners, entities are generally counted as a single investor unless the entity LP (a) was formed for the specific purpose of investing in the fund or (b) is a private investment company and owns 10% or more voting securities of the fund.

Section 3(c)(7)

Section 3(c)(7) is available for issuers whose securities are only owned by persons who are “qualified purchasers.”

This allows a private fund to have unlimited investors so long as it does not engage in a public offering and limits its investors to qualified purchasers.

Whether an LP is a qualified purchaser must be evaluated at the initial investment commitment.

The term “qualified purchaser” includes:

- An individual investor or a family office with at least $5 million in investments.

- The qualified purchaser is an individual or an entity that invests at least $25 million for their accounts or on behalf of other investors.

- Any entity where all owners are qualified purchasers.

The limits imposed by Section 3(c)(1) (as to the number of investors) and Section 3(c)(7) (as to status as a qualified purchaser) do not apply to a fund’s “knowledgeable employees” (i.e., such employees do not count toward the 100 limit).

These individuals have financial knowledge, expertise, and a close relationship with the fund, and therefore do not need the protection of the Investment Company Act.

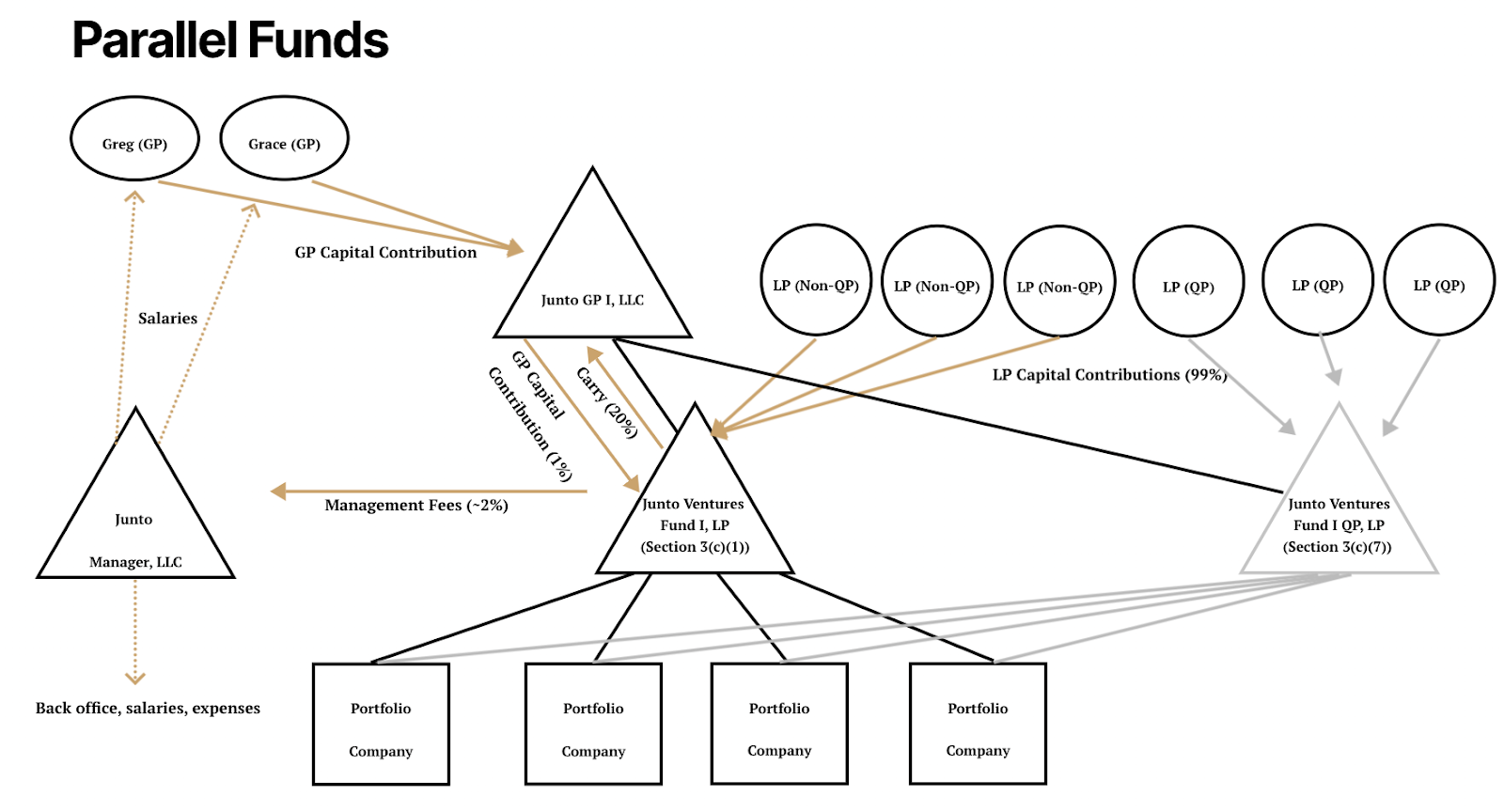

Parallel Funds

In Part II, we discussed parallel funds but focused on the use of parallel funds in the context of non-US LPs.

However, parallel funds are also used to increase the number of LPs eligible to invest in a fund.

For instance, a GP may establish a Section 3(c)(1) fund and a Section 3(c)(7) fund to invest in parallel.

Investment Adviser Act of 1940

Unlike the Securities Act and Investment Company Act, which regulate the fund, the Investment Adviser Act of 1940 (the “Adviser Act”) regulates investment advisers, such as the management company providing investment advisory service to the fund.

Similar to the Securities Act and Investment Company Act, the Adviser Act provides paths to registration (i.e., registered investment advisers or IRAs) but is more often triggered by exemption (exempt reporting advisor or ERAs).

Dodd-Frank amended the Adviser Act to exempt investment advisers to venture capital and other private funds–specifically, the Section 203(l) and Section 203(m) exemptions.

Section 203(l)

Section 203(l) provides that an investment adviser solely to one or more “venture capital funds” is not subject to registration under the Adviser Act.

Generally, a “venture capital fund” is a private fund that:

- Pursues a venture capital strategy;

- Invests no more than 20% of the fund's capital contributions in non-qualifying venture capital investments (e.g., at least 80% of the portfolio is equity and convertible equity);

- Is not significantly leveraged (e.g., does not borrow 15% of fund assets);

- Only issues illiquid securities, except in extraordinary circumstances (e.g., not redeemable except in extraordinary circumstances);

- Is not registered under the Investment Company Act and is not a business development company.

Section 203(m)

Fund managers can also claim an exemption under Section 203(m), which exempts an investment adviser of private funds if such adviser acts “solely as an adviser to private funds and has assets under management in the United States less than $150M.”

Form ADV

An investment adviser relying on Section 203(l) or Section 203(m) may operate as an exempt reporting adviser by filing a truncated version of Form ADV with the SEC (a less robust version of those submitted by RIAs).

Form ADV is not an application, and the SEC does not have the authority to deny an eligible adviser’s ability to take advantage of the exemption.

An ERA must file Form ADV within 60 days of relying on an exemption and file annual amendments within 90 days of the end of each fiscal year.

Part 1A of Form ADV requires information about an ERA’s beneficial ownership, clients, private fund information, employees, disciplinary actions, and certain business practices.

Notably, ERAs do not file Form ADV Part 2, which is for RIAs and requires a “brochure”–a plain-English narrative of its advisory business.

Form ADV must be submitted electronically through the Investment Adviser Registration Depository (IARD).

Like Blue Sky laws, advisers may be required to register or make certain filings under state law.

Other Regulator Regimes

CFIUS

The Committee on Foreign Investments in the United States (“CIFIUS”) is an interagency committee that evaluates certain foreign investments into U.S. businesses and has the authority to mitigate security risks, such as by enforcing divestiture.

Historically, the scope of CFIUS was reserved for defense contractors and controlled technologies under U.S. export laws. However, the 2018 enactment of the Foreign Investment Risk Review Modernational Act (“FIRRMA”) significantly expanded the application of CFIUS.

CFIUS has the authority to review “covered transactions,” which are transactions (e.g., M&A deals, joint ventures, and non-controlling investments) in which a “foreign person” could be deemed to control, directly or indirectly, a U.S. business engaged in matters concerning critical technology, critical infrastructure, or sensitive personal data or otherwise have access to material non-public technical information.

An entity may be considered a foreign person even if it is a U.S. entity and has its principal place of business in the U.S. if a foreign person is deemed to have control (e.g., board representation), access to “material non-public technical information,” or substantial decision-making authority.

Generally, if a transaction is covered and not otherwise exempt, it will be subject to CFIUS review.

CFIUS concerns may impact a VC’s ability to bring on certain GPs or grant increased information or oversight rights to LPs out of concern that such a person may render the fund a foreign person, which could impact the fund’s relationship with a startup (e.g., holding a board seat).

Tax

VC funds are typically taxed as partnerships and subject to partnership tax laws and reporting obligations.

However, many VC funds must also satisfy unique tax requirements to accommodate certain LPs (e.g., non-US investors).

Moreover, most VCs structure their investments to qualify as “qualified small business stock” to receive the tax benefits associated with QSBS.

Sufficit to say that the legal and compliance obligations related to tax are beyond the scope of this post, but we plan on addressing these considerations later.

Conclusion

This concludes our three-part series on starting and operating a venture capital fund.

This last post discussed various legal and compliance issues applicable to VCs (and their LPs).

Specifically, we discussed the most common Reg D exemptions (i.e., Rule 506(b) and Rule 506(c)), the Investment Company Act and the limits on the number of LPs in a fund, and the compliance hurdles of the Investment Adviser Act.

About the Author

(and disclaimer)

Hey, if you like this article, you should follow me on Twitter (I tweet about venture, web3, and sports (with plenty of dad jokes)), check out what we are building, or set a time to chat.

Disclaimer: While I am a lawyer who enjoys operating outside the traditional lawyer and law firm “box,” I am not your lawyer. Nothing in this post should be construed as legal advice, nor does it create an attorney-client relationship. The material published above is only intended for informational, educational, and entertainment purposes. Please seek the advice of counsel, and do not apply any of the generalized material above to your facts or circumstances without speaking to an attorney.