Growing a venture-backed startup is difficult–even if you started on the right foot by initially incorporating as a Delaware C-Corp.

Unfortunately, this difficulty isn’t alleviated for many administrative tasks, such as filing annual reports and paying Delaware franchise taxes.

In fact, around this time of the year, we get many questions from founders asking why their Delaware franchise taxes are $85,000!

This hefty franchise tax bill is because the default tax calculation is based on the “Authorized Shares Method," which calculates taxes based on the number of authorized shares.

For many venture-backed startups is around 10,000,000 authorized shares.

This post cuts through the complexities of calculating and paying your annual Delaware franchise tax bill.

Specifically, we discuss the alternative methods of calculating Delaware franchise taxes, which can cut the bill by thousands or tens of thousands.

Let's Dive In

First, you must locate your Delaware file number, which you can locate by searching with your company’s legal name here.

Once you have located your Delaware file number, you will go to Delaware’s franchise tax page.

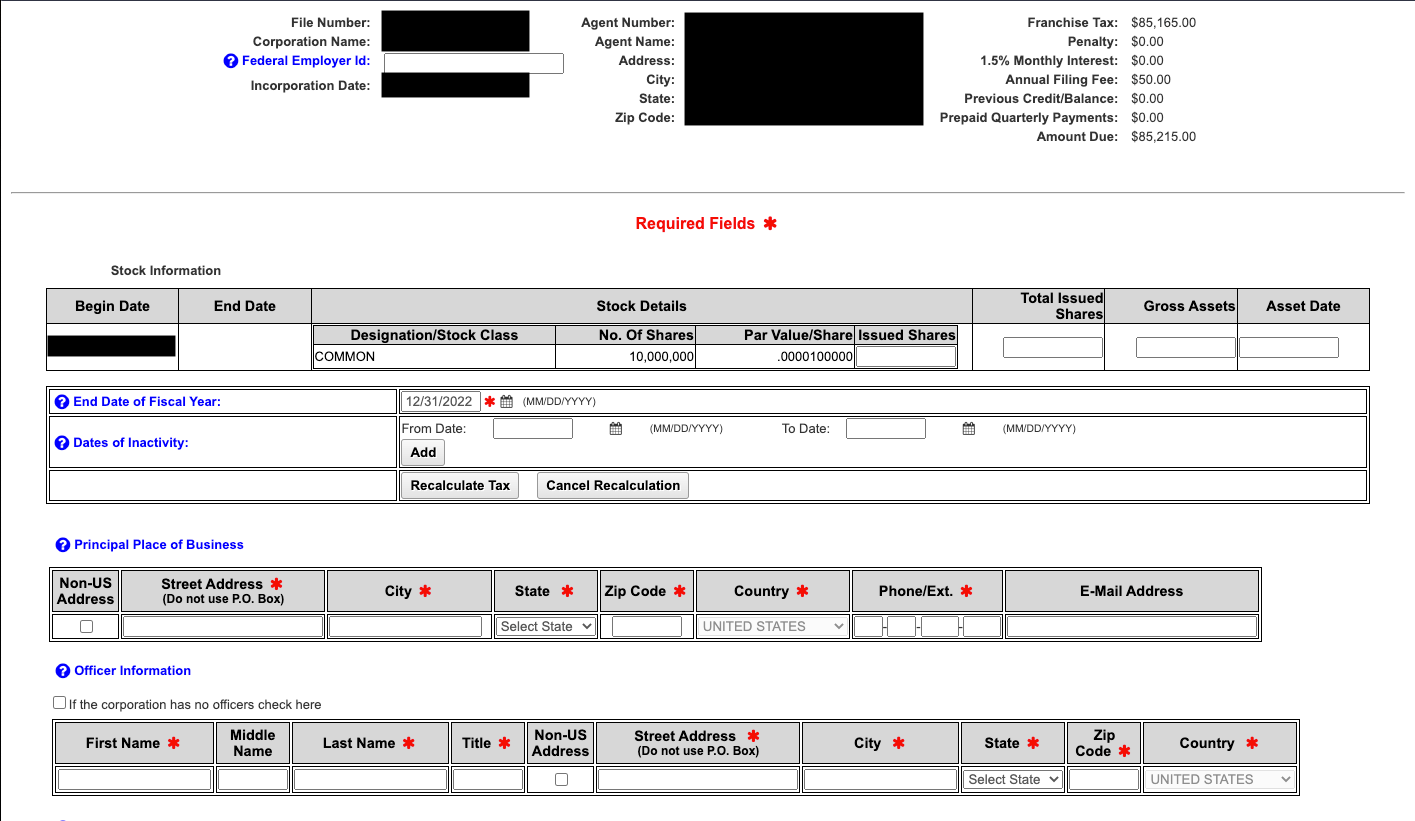

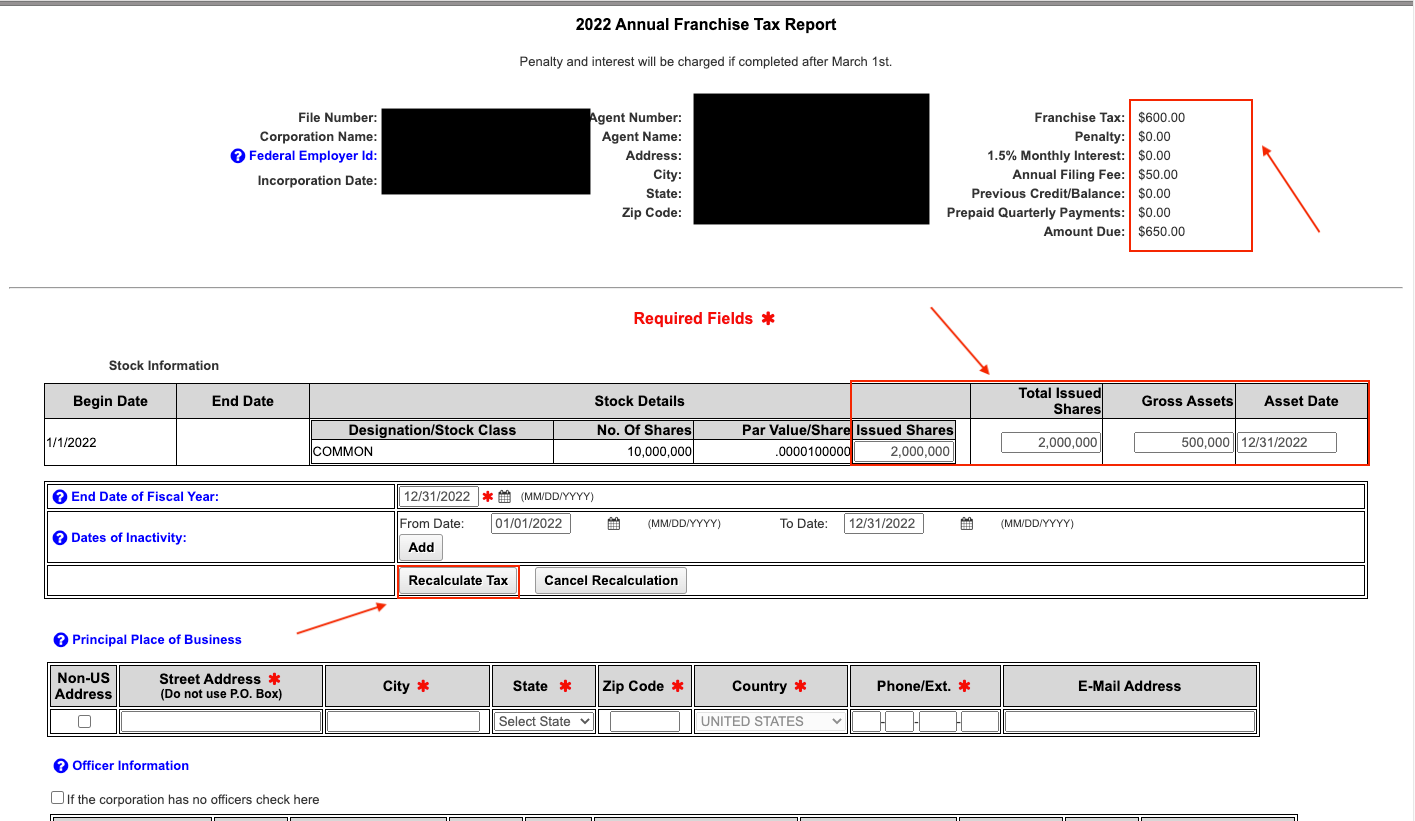

Input your Delaware number, which will take you to a page that looks like this:

Looking at the top right of the page, the franchise taxes are incredibly high!

This is because franchise tax is being calculated based on the “Authorized Shares Method.”

Instead, it is often more beneficial to calculate franchise taxes based on the “Assumed Par Value Method.”

To use the Assumed Par Value Method, you must fill in the red boxes below (i.e., number of issued shares, gross assets, and click the “Recalculate Tax” button).

Make sure you check with our accountant on your Gross Assets.

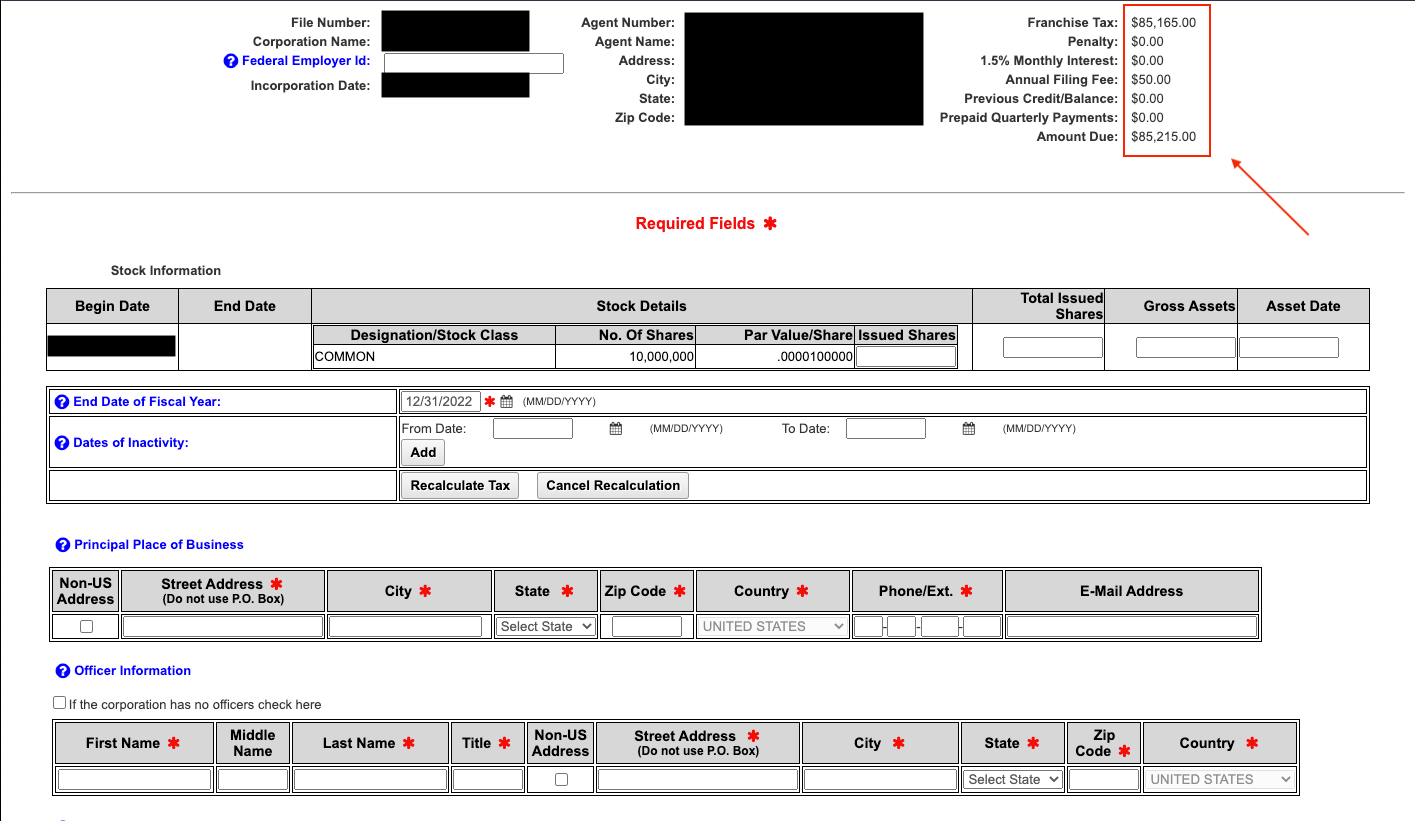

As you can see, by including this information and recalculating the tax, the franchise taxes decline dramatically.

The "Assumed Par Value Capital Method" is used to do this.

This method calculates the franchise tax based on all issued shares, authorized shares, and total gross assets. Here's how it works:

Step 1: Divide Total Gross Assets by Total Issued Shares to get the "Assumed Par Value." Carry this sum to six (6) decimal places.

Issued Shares are those awarded to persons or entities out of the company's Authorized Shares.

Authorized Shares are the total number of shares the company may award as outlined in the company's Certificate of Incorporation.

Step 2: Multiply the Assumed Par Value by the number of Authorized Shares having a par value less than the Assumed Par Value.

Step 3: Multiply the number of Authorized Shares, with a par value greater than the Assumed Par Value, by those Authorized Shares' respective par value.

Step 4: Add the sums obtained in Steps 2 and 3 to get the "Assumed Par Value Capital."

Step 5: Calculate the franchise tax at $400 per every $1,000,000 or portion of Assumed Par Value Capital. Put another way, divide the total Assumed Par Value Capital (if it is over 1,000,000) by 1,000,000, rounding up any partial number by 1. Then multiply that number by $400 to arrive at the appropriate tax.

If Assumed Par Value Capital is under 1,000,000, round up to 1 and multiply by $400 to arrive at the appropriate tax.

Summary

In conclusion, the Assumed Par Value Capital Method is often (but not always) a much better option for calculating Delaware franchise taxes for early-stage, high-growth, venture-backed startups.

This simple tweak to your franchise tax calculation can potentially save your company thousands or tens of thousands of dollars on Delaware franchise taxes.

But remember, consult with your tax and legal professionals to ensure your gross assets and other relevant numbers are correct for these calculations.

About the Authors

(and disclaimer)

Hey, if you like this article, you should follow Shayn, Ben, and Junto on Twitter, check out what we are building, or set a time to chat.

Disclaimer:While we are lawyers who enjoy operating outside the traditional lawyer and law firm “box,” we are not your lawyer. Nothing in this post should be construed as legal or tax advice, nor does it create an attorney-client relationship. The material published above is intended for informational, educational, and entertainment purposes only. Please seek the advice of counsel, and do not apply any of the generalized material above to your facts or circumstances without speaking to an attorney.