We're teaming up with our friends at Sydecar to publish a three-part series on the legal (and non-legal) aspects of starting (and running) a venture capital fund.

Sydecar aims to bring more efficiency to private markets by standardizing how investment vehicles are created and executed. Their products allow capital allocators to launch investment vehicles instantaneously, track funding in real-time, and offer hassle-free opportunities for early liquidity.

Throughout the series, we will discuss: (1) the legal structures and players, (2) the common and important terms, and (3) the regulatory hurdles.

What are VC Funds?

Venture capital funds are used to pool capital from investors and deploy it into companies identified by the venture capitalist.

An investor's investment into the fund ("Fund") is known as a capital commitment and is made in exchange for an interest in the Fund.

Investors do not typically pay capital commitments at the outset or all at once.

Instead, capital calls are made over the Fund's investment period, which is the period in which the VC is authorized to deploy capital (e.g., 3-5 years).

This allows investors to avoid having their money lying dormant while the VC identifies investment opportunities.

Similarly, capital calls are also helpful to the VC, who does not want to start the clock on its internal rate of return by calling capital before it is ready to be deployed.

Structures and Players

As we will discuss throughout this series, there aren't many technical barriers to becoming a VC.

While there are plenty of regulatory hurdles, there are no required licenses, specific education, or testing requirements. A VC isn't even required to be an accredited investor independently.

In fact, the VC may qualify as an accredited investor simply by raising a Fund above $5M or being a knowledgeable employee of the Fund (more on this in Part III).

So far, we've used the term VC generically, but many different people and entities may be considered the "VC."

General Partners ("GP")

The founders of the VC firm are often considered the "VC," but the more precise title is general partner or GP.

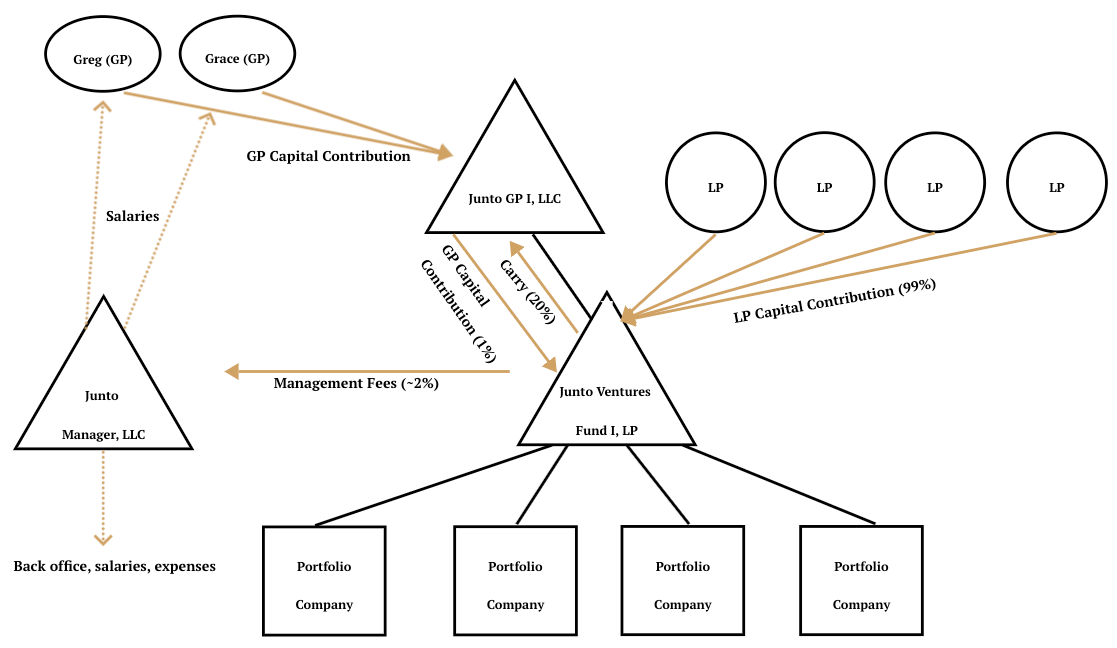

The GPs usually wrap themselves in a legal entity–such as an LLC (e.g., Junto GP I, LLC)- to limit liability and operate through a corporate existence.

The GP designation also denotes its role in the traditional fund structure–as the general partner of a limited partnership.

In the traditional fund model, the Fund is organized as a Delaware limited partnership, which includes a general partner (e.g., GP entity) and one or more limited partners (i.e., the investors).

In a Fund that is formed as a limited partnership, the GP has the power and authority to manage and act on behalf of the Fund, such as making investment decisions, signing contracts (e.g., the Investment Management Agreement with the Management Company), filing tax and regulatory filings on behalf of the fund, and distributing Fund property.

The investors grant broad discretion and authority to the GP in managing the Fund.

However, the Fund's governing documents (in a limited partnership, the Limited Partnership Agreement) do include important restrictions on GP authority without the investors' consent.

For instance, the GP may be limited to making investments consistent with a particular Fund thesis, which may be based on stage (e.g., seed, growth, late-stage), industry sector (e.g., enterprise SaaS, biotechnology, blockchain, clean-tech), or philosophy (e.g., geographic-based).

Limited Partners ("LPs")

The most important players in a Fund are the limited partners or LPs, which are the Fund's investors.

Just as the existence of a startup may depend (at least to some extent) on the involvement of a VC, the VC is as much reliant on its LPs.

Typically, LPs are wealthy individuals, family offices, endowments, funds of funds, pensions, etc.

Many LPs look at VC investments as a piece of their overall investment portfolio (e.g., along with public stocks or bonds).

However, the LPs expect the VC to generate outsized returns with the tradeoff of higher risk.

Along with these expectations, LPs will have certain expectations related to the GP.

For instance, the LPs will expect that the GP has some skin in the game by requiring the GP to contribute at least 1% of the Fund's capital contributions.

This is particularly true for first-time fund managers who may not be able to point to a significant track record to garner LP trust.

Despite contributing almost all of the capital (e.g., 97-99%), LPs do not receive (and do not expect) substantial governance rights.

Instead, the predominant rights of the LPs are economic in nature (e.g., the top tier of the distribution waterfall), which we will discuss in more detail in Part II.

Put simply, LPs rely on the GP and its team to handle the day-to-day operations of the Fund.

Management Company

In addition to the GPs, the Fund (directly and indirectly) relies on the individuals employed or hired by the GP to carry out and manage the Fund and VC firm.

For instance, VC firms often employ analysts, associates, and principals that identify and evaluate investments.

A VC firm may also employ (or outsource) back-office support teams, including accountants, lawyers, and administrative personnel.

Some of these individuals may be granted a portion of the carried interest or carry paid to the GP (e.g., 20% of the profits generated from the Fund after returning capital to LPs (plus any preferred return), more on this in Part II).

This right is usually subject to vesting (more on vesting in other contexts here).

Instead of housing these individuals within the GP entity, the VC often forms a management company (e.g., Junto Manager, LLC) to compensate and employ these individuals.

The GP and the Fund often enter into an "Investment Management Agreement" with the Management Company.

Under the Investment Management Agreement, the Management Company is delegated to sourcing investments and is entitled to the Fund's management fees (more on this in Part II) and reimbursement of the costs and expenses of each Fund.

A traditional (i.e., closed-end) structure is shown below:

The above represents a traditional fund structure.

In recent years, various other structures have emerged with their own nuances, such as rolling funds, evergreen funds, syndicates, and DAO Investment Clubs.

Conclusion

A VC Fund is used to pool capital from LPs, which is then called over the investment period by the GP to be deployed into startups.

Although the term VC is often used generically, there are various players under that umbrella, including the GP, the Management Company, and the other stakeholders of the GP or Management Company (e.g., principals, associates, advisors, back office)–each with a unique role.

In Part II, we will dig deeper into some key terms for starting and running a venture capital fund.

About the Author

(and disclaimer)

Hey, if you like this article, you should follow me on Twitter (I tweet about venture, web3, and sports (with plenty of dad jokes)), check out what we are building, or set a time to chat.

Disclaimer: While I am a lawyer who enjoys operating outside the traditional lawyer and law firm “box,” I am not your lawyer. Nothing in this post should be construed as legal advice, nor does it create an attorney-client relationship. The material published above is intended for informational, educational, and entertainment purposes only. Please seek the advice of counsel, and do not apply any of the generalized material above to your facts or circumstances without speaking to an attorney.