Venture capital is known for fueling innovation and disrupting traditional industries, yet raising a venture fund has remained notoriously complex and expensive. However, a new wave of legal and technological solutions is poised to change the game for emerging fund managers.

In this blog post, we'll explore the hurdles associated with raising and operating a venture fund and how Sydecar's innovative Fund+ structure simplifies fund formation, reduces costs, and makes venture capital more accessible to a broader range of investors and fund managers.

Barriers to Entry

It surprises many that there are no technical barriers to becoming a venture capitalist.

However, the process of raising a venture fund comes with significant hurdles. Raising and operating a venture fund can range between $50,000 and $100,000 in legal fees. These astronomical fees act as barriers to entry, preventing all but the most wealthy from gaining access to this valuable asset class.

So, why is raising a fund so expensive?

The diverse nature of LPs in a traditional fund structure often requires specific tailoring and accommodations. For instance, institutional investors, foreign LPs, sovereign wealth funds, and pension plans often require tax and regulatory accommodations that do not apply to high-net-worth individuals and family offices. Additionally, certain venture capital strategies may necessitate more nuanced structures and legal documents. For instance, if a fund invests in offshore companies or follows a sector-specific investment strategy, legal documents may need to be drafted to address these nuances.

Similarly, the legal and regulatory framework surrounding the venture capital space is ever-changing–so there is undoubtedly a level of required maintenance.

Nuance and accommodation are not unique to the venture capital industry. The venture space has taken significant steps to standardize how capital gets deployed into startups (e.g., SAFEs, the Series Seed, and the National Venture Capital Association’s model documents).

However, the industry has failed to bring a standardized approach to fund formation and operations–at least in model documents. Even the Institutional Limited Partners Association’s model limited partnership agreement is tailored toward buy-out funds rather than traditional venture capital funds.

Emerging VC backoffice complexity is a hell of a thing. The problem for most new managers is that there is an absence of what 'good' looks like when selecting fund admin, tax, and audit partners.

— Eric Bahn 💛 (@ericbahn) January 12, 2023

I think I want to spend more time this year tweeting what I've learned so far.

As a result, emerging fund managers often rely on bespoke legal documents that can differ dramatically depending on the counsel involved or minor divisions in structure or LP base. This lack of uniformity has made the upfront costs of raising and operating a venture fund prohibitive for many emerging fund managers.

The costs of raising a venture fund is only one of the challenges that emerging fund managers face. There are other more significant challenges, such as attracting and retaining LPs, implementing effective strategies, and generating returns.

Emerging fund managers should focus on these challenges to better position their funds instead of combining through a PPM or issuing K-1s.

The Opportunity and Benefits of Standardized Fund Docs

For venture capital to grow as an asset class, removing some of these barriers to entry is critical.

Ironically, an industry that rewards itself for finding technological inefficiencies in large markets have fallen far behind in technological innovation. Only recently have companies like Carta moved cap table management from siloed spreadsheets to the cloud, AngelList’s leverage of a social network to raise a syndicate, and now, Sydecar to provide fund formation and operation solutions.

As lawyers, we’ve seen firsthand the frustrations of an industry that views innovation as a threat. However, we see these tools as a tremendous value that will allow us to spend more time doing what we enjoy most–helping entrepreneurs build companies.

Emerging technologies not only reduce the cost of legal fees but also help streamline the fundraising and operation process, attract and retain investors, and can lead to better investment outcomes.

Enter Sydecar

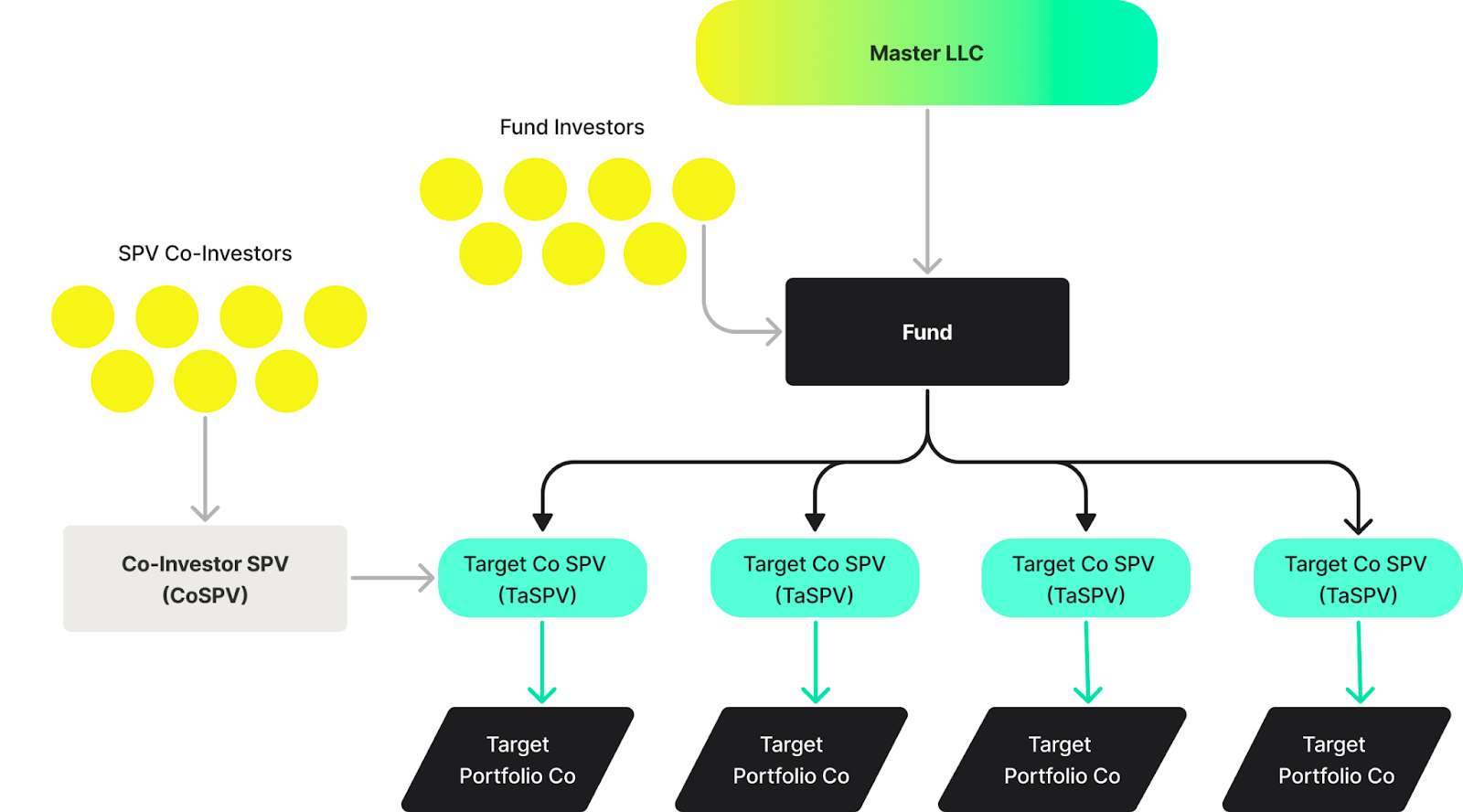

Sydecar's Fund+ structure incorporates concepts from the syndicate and special purpose vehicle (“SPV”) models. Specifically, Sydecar leverages the flexibility of series LLCs to implement a structure where a fund manager only needs a single parent LLC.

Under the parent LLC, a series of the parent is formed as a quasi-feeder fund. Although LPs invest directly into the fund, the fund does not directly invest in portfolio companies. Instead, Sydecar establishes an SPV in which a portion of the fund’s capital flows into and is deployed by the SPV into a portfolio company.

Sydecar's fund structure is simplified, with only two entities necessary instead of the typical three for a venture fund. Sydecar creates the fund, while the fund manager establishes the management/GP entity that receives management fees and carry from the fund.

This approach allows a fund manager to bring outside LPs for specific investments. Because outside investors are not required to invest in the main fund, this provides an opportunity for emerging fund managers to expand their base of LPs.

This also allows LPs to “test the waters” in their exposure to emerging fund managers. Moreover, this approach may address unique regulatory and tax concerns for limited partners.

Sydecar's Fund+ structure is ideal for emerging fund managers who have made investments in the past, whether as angel investors, syndicate leads, or investment professionals in traditional funds.

By leveraging this structure, fund managers can significantly reduce upfront costs and complexity associated with traditional fund structures.

Overview of Terms

Sydecar’s Fund+ includes subscription agreements and a Limited Liability Company Agreement (“LLCA”) for the parent, the fund, and associated SPVs. The highlights of the fund LLCA include:

- Role of Sydecar. Sydecar acts as the fund administrator and acts on behalf of the fund manager. This delegation allows Sydecar to handle regulatory and tax filings, accept subscriptions, make distributions, and otherwise handle other administrative matters.

- Carried Interest and Management Fees. The fund manager can use the subscription agreement to designate the applicable carried interest and management fees on an LP-by-LP basis.

- Fund Expenses. The LLCA recognizes that fund expenses, including formation and operating expenses, will be paid out of LP capital contributions.

- Co-Investment Rights. The fund manager retains the right to allow fund LPs or outside investors to co-invest alongside the fund in portfolio investments through the portfolio SPVs.

- Side Letters. The fund manager retains the right to enter into side letters with LPs to accommodate tax or regulatory concerns or otherwise offer terms that do not apply to other investors. This provides the fund manager with flexibility in accommodating LPs.

Summary

In summary, the Sydecar Fund+ structure offers emerging fund managers a unique and flexible approach to fund formation that can significantly reduce upfront costs and complexity associated with traditional fund structures.

By leveraging series LLCs and SPVs, fund managers can provide investors with a clear understanding of the fund and its investments while also accommodating unique regulatory and tax concerns for LPs.

Additionally, by partnering with Sydecar, fund managers can streamline their back-office operations and focus on investment activities while benefiting from the expertise of experienced legal and administrative professionals.

With the right legal and administrative support, emerging fund managers can focus on identifying and investing in promising startups rather than being bogged down by the complexity and costs associated with traditional fund structures.

About the Author

(and disclaimer)

If you like this article, you should follow me on Twitter, check out what we are building, or set a time to chat.

Disclaimer: While I am a lawyer who enjoys operating outside the traditional lawyer and law firm “box,” I am not your lawyer. Nothing in this post should be construed as legal advice, nor does it create an attorney-client relationship. The material published above is only intended for informational, educational, and entertainment purposes. Please seek the advice of counsel, and do not apply any of the generalized material above to your facts or circumstances without speaking to an attorney.